USDA Predicts "King Soybean" by 2019

TOPICS

Wheat

photo credit: Arkansas Farm Bureau, used with permission.

John Newton, Ph.D.

Former AFBF Economist

On Nov. 28, 2017, USDA released several tables previewing the annual long-term Agricultural Projections to 2027 (the complete projections will be released in February 2018). These early-release tables provide USDA estimates on the supply and demand for agricultural commodities through 2017 and take into consideration macroeconomic conditions, GDP growth, population growth and farm policy, among other factors. USDA assumes in the projections normal weather and no significant supply or demand disruptions, i.e. a business-as-usual environment.

Acreage Changes

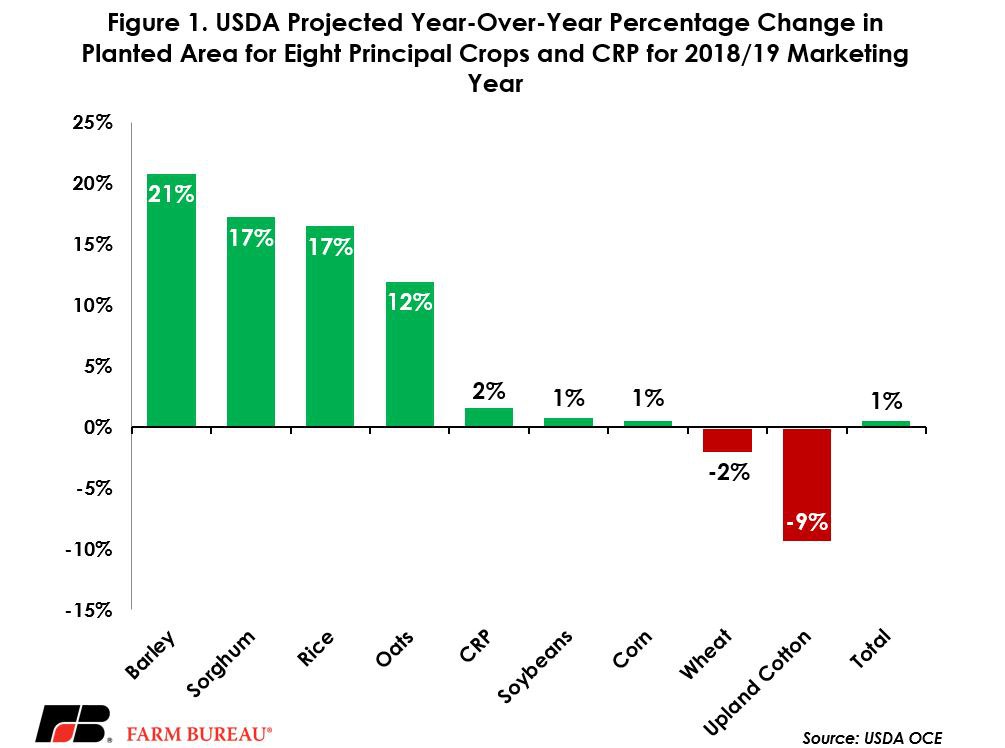

One of the most anticipated items from the early-release is USDA’s projections for planted area in 2018. During 2017 the total planted area for the eight principal crops and conservation reserve program was 275.8 million acres. For 2018, USDA projects planted area to increase for all crops except upland cotton and wheat, with a total acreage gain of 1.8 million acres to 277.6 million acres, Figure 1. Then, from 2019 to 2027, USDA projects planted area and CRP land to remain steady between 276 and 278 million acres – slightly lower than the 280-million-acre-average over the last decade.

Of the acreage change projected in 2018, barley is projected to add 519,000 acres to 3 million acres. Sorghum acres are projected to increase by 991,000 acres in 2018 to 6.7 million acres. Rice planted area is projected to increase 413,000 acres to 2.9 million acres. Oat acreage is expected to increase 312,000 acres to 2.9 million acres. CRP acres are projected to increase modestly but will remain below the Congressional cap of 24 million acres. Soybean acres and corn acres are projected to increase by 793,000 acres and 571,000 acres, respectively, to 91 million acres each. If realized, 91 million acres would be a new record-high for soybean acreage. Wheat acres are expected to decline for a fourth year in a row, down 1 million acres to 45 million acres – the lowest level since U.S. first began recording acreage data in 1919. Finally, upland cotton acres are projected to decline 1.2 million acres to 11.2 million acres in 2018.

King Soybeans

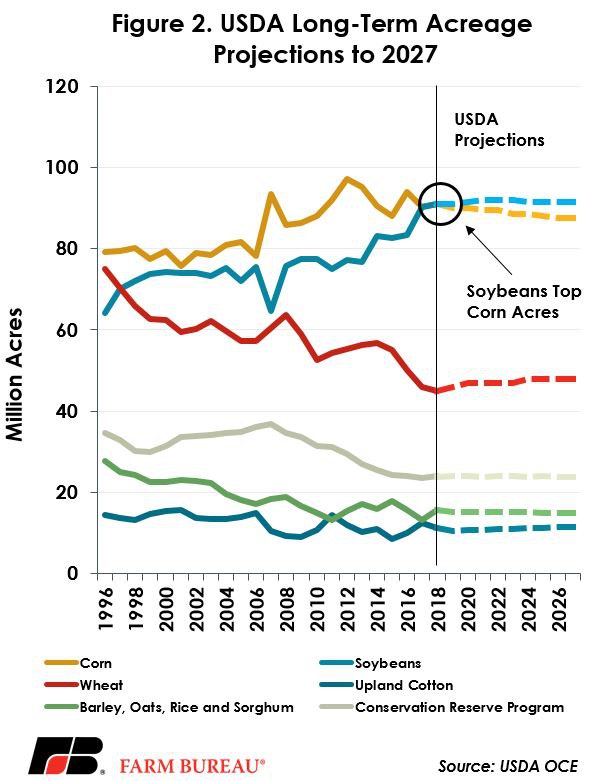

While in aggregate USDA projects acreage to increase slightly in 2018, the biggest takeaway is that USDA projects soybean acreage to top corn acreage beginning in 2019 and continuing through 2027. 2018 soybean plantings are projected at 91 million acres, up 793,000 acres from 2017 or approximately 1 percent. Corn acres in 2018 are also projected at 91 million acres, up 571,000 acres or approximately 1 percent. By 2019 however, soybean acres are projected at 91 million acres while corn acres are projected at 90 million acres. If realized, this would be the first market-driven acreage shift that resulted in more soybean acres planted than corn, i.e. King Soybeans, Figure 2.

There are a number of reasons for soybean acreage to continue expanding. The primary reason being demand for soybeans, soybean oil and soybean meal from China. A recent Market Intel reviewed China’s Insatiable Demand for Soybeans. For now, the U.S. is the number one producer of soybeans, but Brazil is a close second. Combined, Brazil and Argentina produce approximately 2 billion more bushels than the U.S. Another Market Intel reviewed South American soybean production trends, Is it too Late for U.S. to be Crowned ‘Soybean King’?

Implications

Chinese demand for soybeans, from North and South America, has driven the rapid expansion in soybean planted area. U.S. producers responded to these market signals by increasing soybean production by 130 percent since 1990. Brazil and Argentina have been much more aggressive, expanding production by 579 percent and 396 percent, respectively. USDA’s most recent projections confirm U.S. producers will continue to respond to Chinese demand and as a result, soybeans are likely to be the largest field crop planted in the U.S. by 2019.

A lot of uncertainty remains before planting decisions are ultimately made. Improvement in the global economy could increase demand for grains and oilseeds, pushing stocks lower than anticipated and pushing prices higher. Higher prices could result in acreage shifting into crops with a more profitable per acre return.

The black swan events that could roil grain markets and alter planting decisions include withdrawal from existing trade agreements (30 percent of corn exports go to NAFTA countires compared to 7 percent for soybeans), a slower pace of consumption, favorable growing conditions in South America and a strong dollar. This does not include what could happen in 280 characters or less, i.e. blue swan events.

These metrics are important to monitor for evaluating planting decisions in 2018 and marketing the 2017 crop. The next opportunity to review potential acreage decisions will come in the March 2018 Prospective Plantings report.

Trending Topics

VIEW ALL