USDA Forced to Rebalance October WASDE After September Grain Stocks Report

TOPICS

Wheat

photo credit: Arkansas Farm Bureau, used with permission.

Shelby Myers

Former AFBF Economist

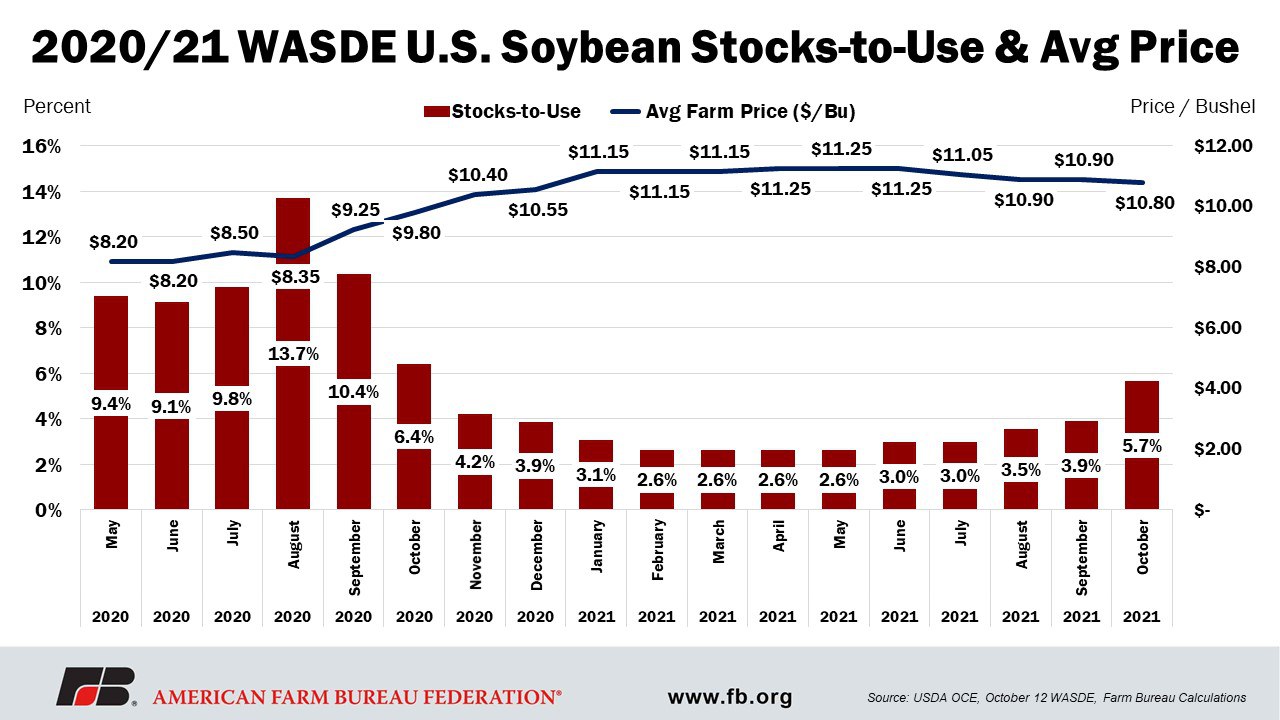

Released on Sept. 30, USDA’s Quarterly Grain Stocks Report showed that as of Sept. 1 old-crop corn and soybean inventory levels had dropped, compelling USDA to update supply and demand expectations in the October World Agricultural Supply and Demand Estimates, released on Oct. 12. Much higher-than-expected soybean stocks and the subsequent adjustments made for old and new crop supply and demand pushed soybean prices for the 2020/21 marketing year average and the 2021/22 marketing year down sharply.

Updated Soybean Supply and Demand Expectations

In the September Grain Stocks Report, soybean ending stocks for the 2020/21 marketing year were increased by 81 million bushels, up 46% from the 175 million bushels USDA originally had pegged to 256 million bushels. This revision still puts soybean ending stocks about 51% behind 2019 soybean stocks.

The October WASDE reflected the changes USDA made to the 2020/21 old soybean crop estimates in subsequent soybean planted acres, harvested acres, yield and production. U.S. soybean production was revised up 80.8 million bushels to 4.2 billion bushels. This uptick in production is attributed to increased planted soybean area, which was revised higher to 83.4 million acres, up 300,000 acres. Similarly, harvested area was bumped up to 82.6 million acres from 82.3 million acres. Also, USDA reports a yield boost from 50.2 bushels per acre to 51 bushels per acre.

Soybean demand was adjusted, with 1 million bushels in increased crushing and a 5 million-bushel increase in exports. The largest adjustment occurred in soybean residual, which was lowered by 7 million bushels, dropping 175% from 4 million bushels to -3 million bushels from September to October, which helps account for the changes to soybean stocks. The increase in stocks pushed the stocks-to-use ratio from 3.9% last month to 5.7% and pushed prices down. The average farm price for soybeans for the 2020/21 marketing year was lowered from $10.90 per bushel to $10.80 bushel.

For the new 2021/22 marketing year, soybean production expectations are increased slightly with a yield bump from 50.6 bushels per acre in September to 51.5 bushels per acre in October, which is slightly up from analysts’ expectations that yield would be closer to 51.1 bushels per acre. The yield increase pushes production expectations for this year’s soybean crop to 4.45 billion bushels, up 5.5% compared to 2020. If that size crop comes to fruition, it will be the U.S.’ largest soybean crop on record.

Given those expectations, USDA this month lowered the estimate for soybean imports to 15 million bushels from 25 million bushels in September. When the 2021/22 marketing year estimates were first published, the tighter margins implied that the U.S. would need to import more soybeans and in May USDA estimated imports of 35 million bushels. The soybean supply increases combined with the 81-million-bushel increase in carry-over stocks put total soybean supply at 4.7 billion bushels, a 3.2% increase compared to September, which is just behind the 4.8-billion-bushel record the U.S. held in 2018.

Despite record soybean production, the only expected increase in 2021/22 soybean demand is in soybean crushing, up 10 million bushels from September to 2.19 billion bushels. Exports for the newest soybean crop are still not estimated to be anywhere near 2020’s peak of 2.265 billion bushels. USDA kept 2021/22 exports in October at 2.09 billion bushels, about 7.7% behind 2020.

With little change made to 2021/22 soybean use and an increase in soybean supply, margins are much looser. Soybean stocks for the 2021/22 marketing year increased 73% this month, going from 185 million bushels to 320 million bushels. The stocks-to-use ratio moved upward from 4.2% to 7.3% this month, while prices dipped from $12.90 per bushel last month to $12.35 per bushel in October.

Updated Corn Supply and Demand Expectations

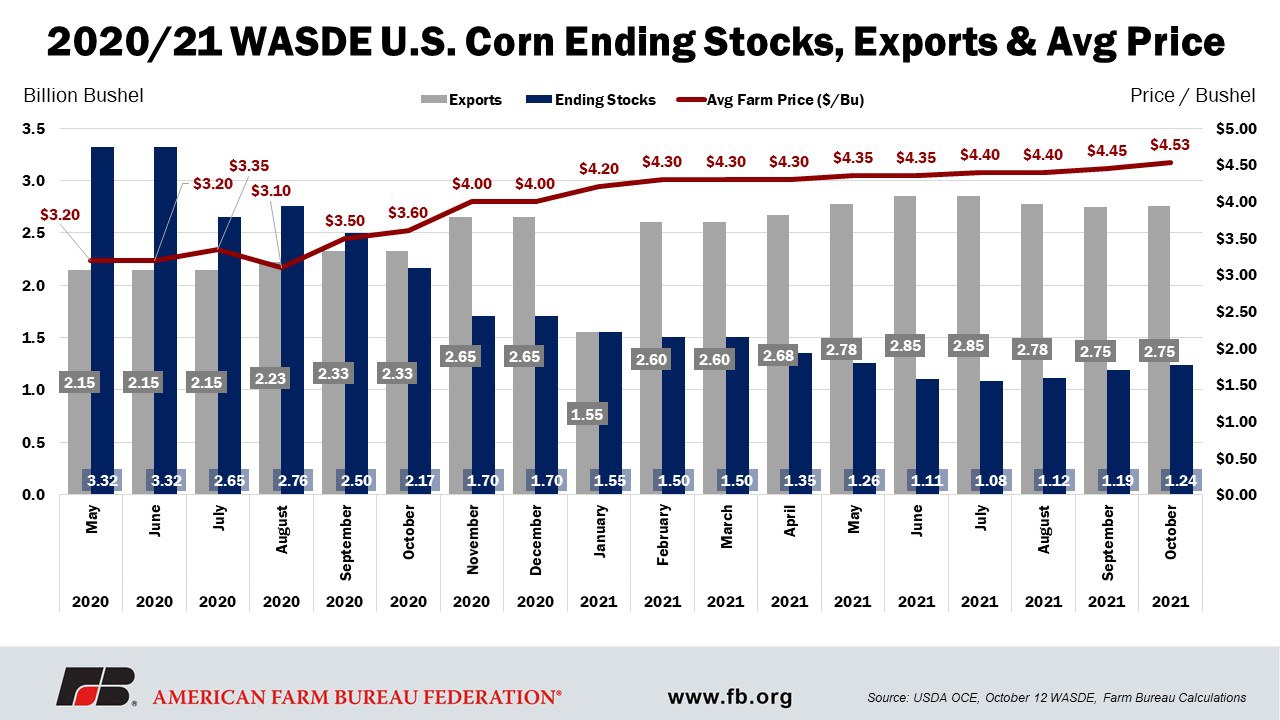

For the 2020/21 marketing year, corn ending stocks were revised up from 1.187 billion bushels to 1.24 billion bushels, an increase of 6% and up from analysts’ expectations of 1.15 billion bushels. This estimate is still about 36% lower than 2020 and close to 2013 levels when the corn price for the average marketing year was around $4.46 per bushel.

However, the increase in corn stocks was not due to an increase in corn production. USDA revised estimates for U.S. corn production for 2020, lowering it by 71 million bushels to just above 14 billion bushels, but still up about 4% compared to 2019. This was influenced by a change to the planted area, which was lowered by 100,000 acres to 90.7 million, and a revision to harvested acres, now pegged at 82.3 million acres, down 200,000 acres compared to estimates USDA provided earlier in the year. USDA is also attributing the slightly lower yield to a down-tick in production, with 2020/21 yields decreasing from 172 bushels per acre to 171.4 million bushels.

USDA did make changes to 2020/21 domestic corn use. Feed and residual use had the largest demand revision, lowering by 128 million bushels to just under 5.6 billion bushels, a decrease of 2.2% from estimates in September. Ethanol use was lowered slightly, as was food, seed and industrial use. Domestic corn use overall decreased a total of 129 million bushels in October when compared to September WASDE estimates. The slight increase in corn exports this month was not nearly enough to offset any domestic changes. The 2020/21 corn stocks-to-use ratio increased from 7.9% to 8.3%, still significantly behind the 13.7% stocks-to-use ratio in 2019. USDA increased the average farm corn price from $4.45 per bushel in September to $4.53 per bushel this month.

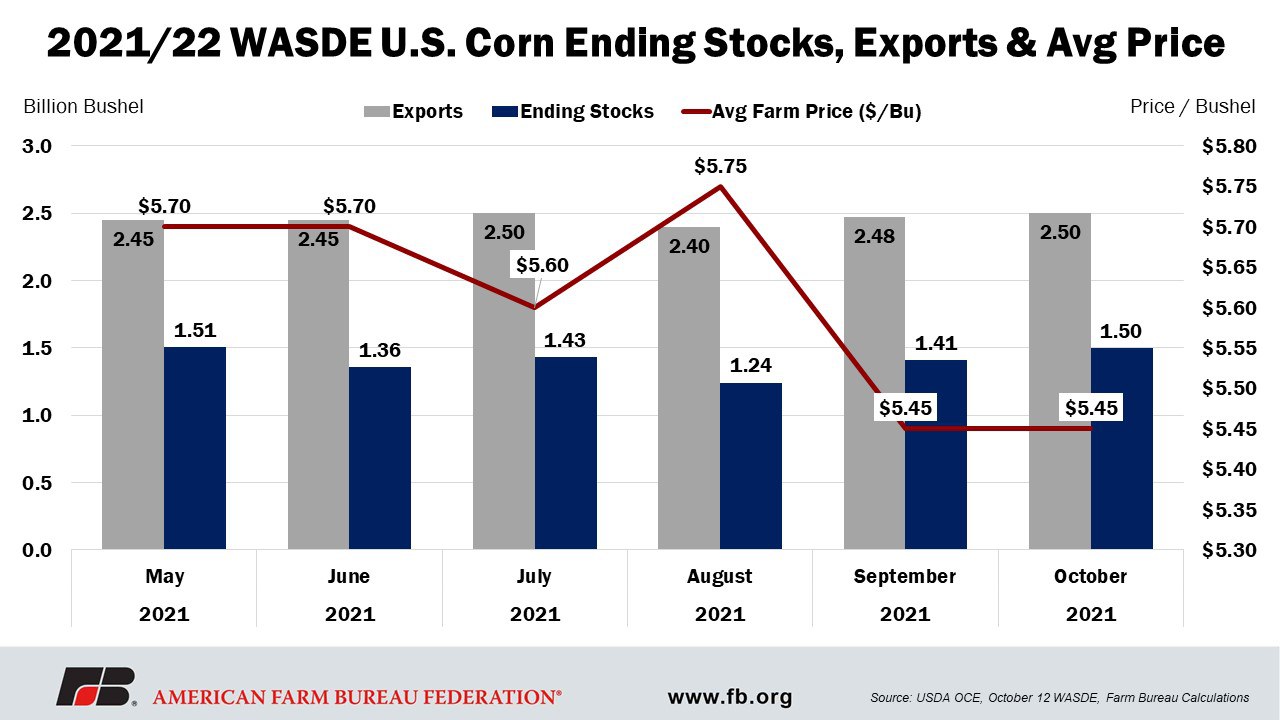

There was a minor increase in yield for new corn crop for the 2021/22 marketing year, rising from 176.3 bushels per acre to 176.5 bushels per acre, from the opposite of analysts’ expectations for corn yields to be revised downward to 176bushels per acre. The best yield on record is 176.6 bushels per acre, which occurred in 2017. The increase to yield and added carry-over stocks from 2020 pushes corn supply upward to 16.2 billion bushels, just about 72 million bushels up from last month.

USDA made minor changes to 2021/22 corn demand. For corn feed and residual, USDA lowered the estimate by 50 million bushels from 5.7 billion bushels to 5.65 billion bushels but increased food, seed and industrial use by 5 million bushels. Corn exports were adjusted upward by 25 million bushels, now reaching 2.5 billion bushels, which would be the second-largest corn export amount behind 2020 corn exports of 2.75 billion bushels. Ending stocks for the 2021/22 corn marketing year were increased by 92 million bushels to reach 1.5 billion bushels, up 21% compared to 2020 ending stock estimates. The stocks-to-use ratio increased from 9.5% last month to 10.1% in October, while the average corn price remained neutral at $5.45 per bushel.

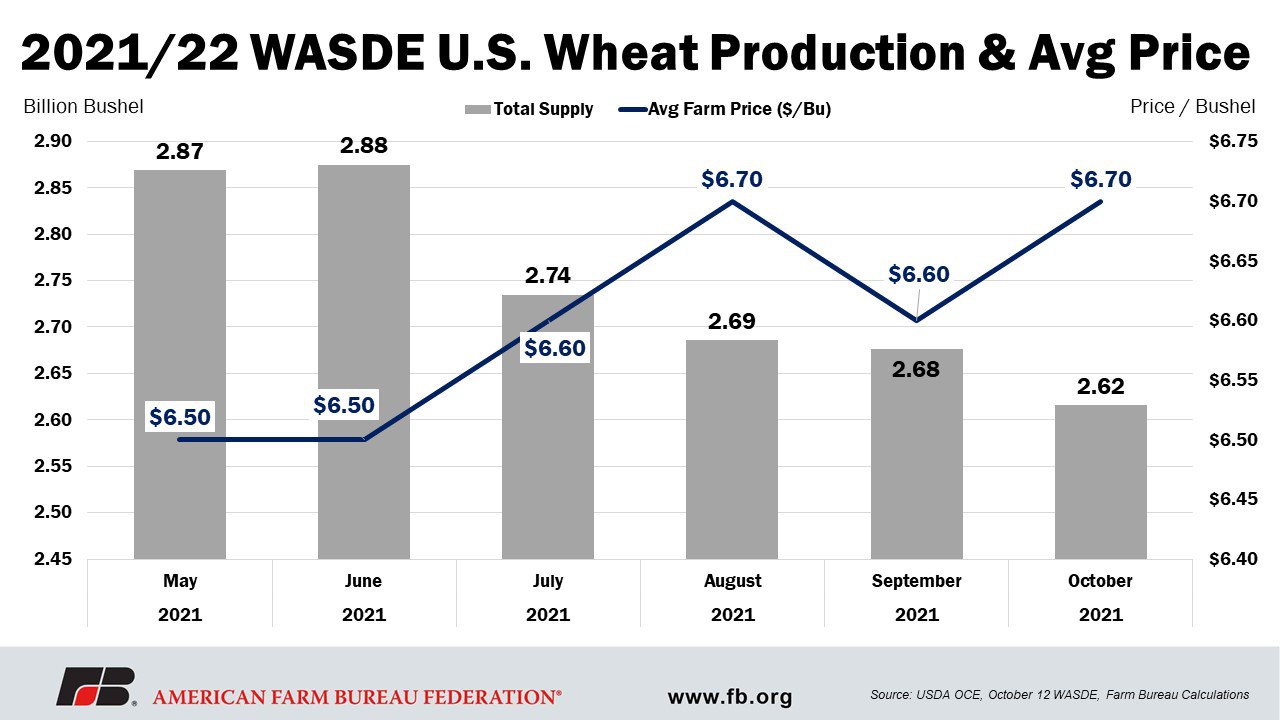

Updated Wheat Supply and Demand Expectations

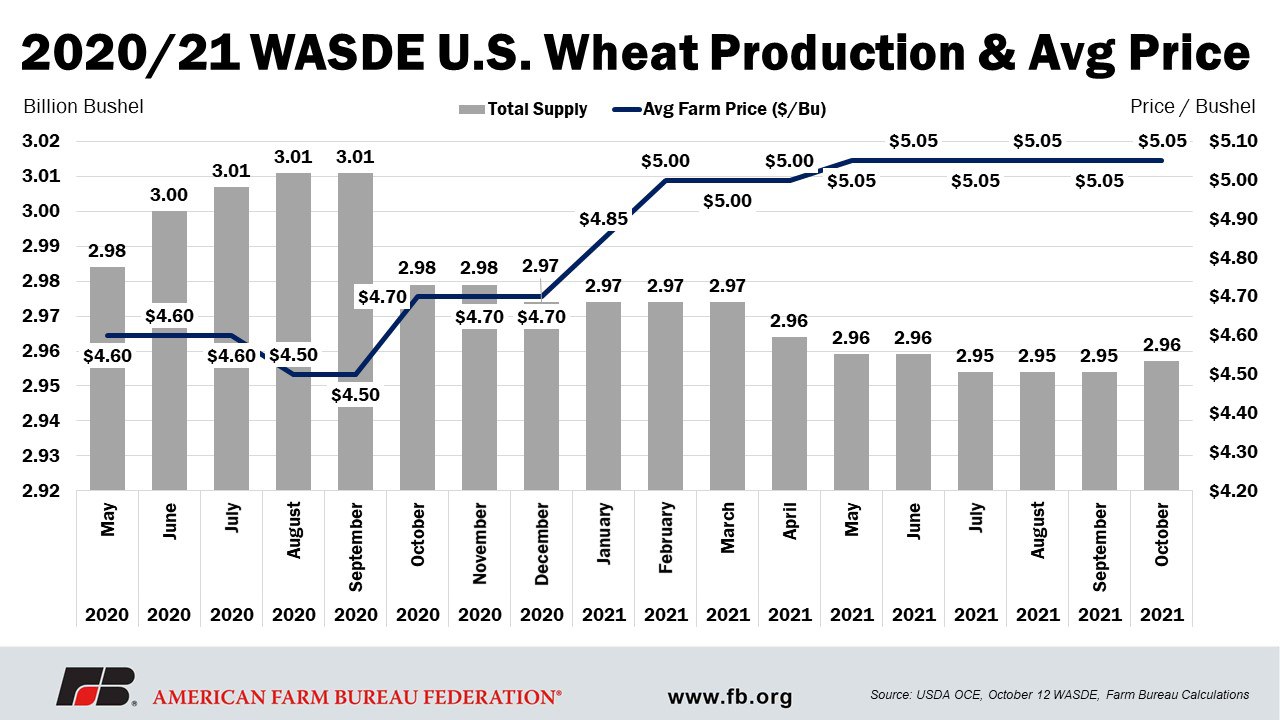

For the 2020/21 marketing year, USDA increased wheat planted area by 200,000 acres, moving from 44.3 million acres to 44.5 million acres, which puts the estimate about 2% behind the planted area in 2019. USDA also increased the wheat harvested area by 100,000 acres, moving it from 36.7 million acres to 36.8 million acres. The increase in the productive area pushed wheat production upward slightly to 1.8 billion bushels and increased overall supply by 3 million bushels to just under 3 billion bushels of wheat.

For 2020/21 wheat use, USDA increased seed use by 5%, moving from 61 million bushels to 63 million bushels, but decreased food and residual use by 2%, moving from 97 million bushels to 95 million bushels. These minor adjustments increased total wheat use by 1 million bushels.

The resulting ending stocks for 2020/21 wheat are pegged at 845 million bushels, which is 18% behind levels in 2019 when wheat ending stocks were above 1 billion bushels. The stocks-to-use ratio for the 2020/21 wheat crop continues to sit at 40%, with the average farm price at $5.05 per bushel.

For the 2021/22 marketing year, wheat stock carry-over is at its lowest point since 2014, but production is expected to be slightly lower given dryer than normal weather conditions. USDA adjusted harvested area lower by 2%, moving from 38.1 million acres to 37.2 million acres, despite an estimated 46.7 million acres of planted wheat, the highest amount since 2018. USDA also lowered wheat yields slightly, moving from 44.5 bushels per acre to 44.3 bushels per acre. The overall result lowers wheat production by 51 million bushels, moving from 1.7 billion bushels to 1.64 billion bushels. USDA also further reduced global wheat imports into the U.S. to 125 million bushels after a reduction last month from 145 million bushels in August to 135 million bushels. The overall impact to supply in 2021/22 is a reduction of 50 million bushels, down 2% compared to September, moving from 2.67 billion bushels to 2.61 billion bushels, the lowest U.S. wheat supply since 2006.

On the demand side for 2021/22 wheat use, USDA decreased feed and residual use by 25 million bushels, going from 160 million bushels in September to 135 million bushels in October, a decrease of 16%. This use category is small compared to other domestic wheat uses and only lowers domestic use by 2% on the balance sheet, moving from 1.18 billion bushels to 1.16 billion bushels.

The changes to supply and demand lower ending stocks to 580 million bushels this month, down 6% compared to last month when wheat ending stocks were 615 million bushels. This would be the smallest amount of wheat ending stocks the U.S. has held since 2013’sending stocks of 590 million bushels. Before that, it would be 2007, when ending stocks were 306 million bushels. The stocks-to-use ratio for 2021/22 wheat currently sits at 28%, which is the lowest level since 2013 when the stocks-to-use ratio was 24%. USDA has this month’s wheat price at $6.70 per bushel, up from $6.60 per bushel last month.

Summary

USDA’s WASDE 2021/22 marketing year domestic balance sheets for corn and soybeans reflected the big surprises in the September Grain Stocks quarterly report. Major adjustments were made to reflect those survey results, particularly for soybeans as 2020/21 ending stocks rose sharply and demand factors were adjusted. However, the impact to the new marketing year, when record soybean production is expected, means much higher than originally reported soybean supplies with little demand change, thus increasing stocks in both marketing years and slowing price increases.

For corn, the increase to old corn stocks will carry over into the new marketing year with increased corn yields. If demand for the new crop year remains stagnant and harvest is not interrupted by weather, prices could drop.

U.S. wheat is pegged to have its lowest supply since 2006 and ending stocks are being pushed to their lowest level in almost a decade, just as an overall reduction in global wheat stocks ripples through, which could help drive wheat prices even higher. With estimates this month implying more grain than expected, except in wheat, there is little worry over too-low corn and soybean stocks. The next WASDE, published on Nov. 9, will likely reflect more robust yield estimates as harvest progresses.