Unwrapping USDA’s New Dairy Processing Cost Study and How it Could Impact Make Allowances

TOPICS

USDA

photo credit: Ohio Farm Bureau, Used With Permission

Daniel Munch

Economist

USDA recently released the Cost of Processing in Cheese, Whey, Butter and Nonfat Dry Milk Plants study, which was commissioned through the University of Wisconsin to update and review the costs of production for dairy processing plants. The study provides new weighted average costs of production of the various types of cheddar cheese, butter, whey and nonfat dry milk for processing plants in the U.S. These costs are often used as a basis for evaluating and adjusting make allowances. This Market Intel reviews the current status of make allowances and discusses the results of the study and its possible implications on future milk pricing calculations, which dictate many dairy farmers’ bottom lines.

Background

A review of milk pricing regulations was provided in a previous Market Intel and can be accessed here: How Milk Is Priced in Federal Milk Marketing Orders: A Primer. As described in the article, milk prices regulated by Federal Milk Marketing Orders (FMMOs) are determined based on end-product pricing formulas. These formulas use wholesale prices for butter, cheese, dry whey and nonfat dry milk to determine milk component values for butterfat, protein, other solids and nonfat solids, as well as the classified value of milk. These end-product pricing formulas include a fixed deduction from each product price called a make allowance, i.e., a processing credit, as well as yield factors for turning raw milk components into finished dairy commodities. In general, any increase in make allowances would increase the deduction to cover processors’ cost, decreasing dairy farmers’ take-home pay in the short-run. A decrease in make allowances would have the opposite effect on dairy farmers’ pay.

Make allowances are based on an estimate of the costs associated with converting a hundredweight of raw milk into commodity dairy products, including butter, cheese or dry milk powder, and are intended to be large enough to encourage the construction and maintenance of processing capacity. The yield factor is an estimate of how much product can be produced from a certain quantity of milk components. The current make allowances and yield factors are as follows:

Make allowances were last modified in 2007 following a USDA Class III and IV make allowance hearing. The dairy farmer and company perspectives on make allowances and yield factors submitted in relation to this hearing are found here: Class III/IV Price Make-Allowances – Comments and Exceptions. Discussed during the hearing was whether a 2006 Cornell Program on Dairy Markets and Policy (CPDMP) survey of manufacturing costs and a 2006 California Department of Food and Agriculture (CDFA) survey should serve as the basis for determining if changes needed to be made to then-current processing costs. The current make allowances for butter and nonfat dry milk (NFDM) were computed by taking a weighted average of the CDFA and CPDMP surveys using national commodity production as the weights and adjusting for USDA-defined marketing costs. The dry whey make allowance was solely based on the CPDMP 2006 survey and adjusted for USDA-defined marketing costs while the cheese make allowance was solely based on the CDFA 2006 survey and adjusted for USDA-defined marketing costs.

The following table shows the difference between the 2006 cost study results values and currently enforced make allowances. Note that, across the board, the current make allowance ended up being higher than the 2006 cost study results, revealing the impact of the hearing process on final values. For ease of comparison to current dairy farmer milk checks, the rest of this article uses current make allowances as a base value.

Results of New Dairy Processing Cost Study

The study released by USDA on Feb. 14 provides new weighted average costs of production for cheddar cheese, butter, whey and NFDM for processing plants based on surveys of 61 plants across the U.S. In short, the study suggests increases in current make allowances across all dairy commodity categories, except butter, would be needed to reflect higher processor costs related to labor, utilities, processing inputs, packaging, general administration and returns on investments.

The following table displays current make allowances and the corresponding weighted average cost values estimated in the new report. Keep in mind that values presented in the study are not the sole determinant in any future updates or changes to make allowances but have been used as a base reference point for FMMO hearings in the past. Butter is the only commodity estimated to have a reduction in cost of production, about minus 3 cents per pound, while NFDM had the largest jump with an increase of 13 cents per pound.

Through the end-product pricing formula, these commodity-based values can be converted into the equivalent make allowance for the four components – protein, butterfat, nonfat solids and other solids – as presented here:

Then, using the end-product pricing formulas, the make allowances can be converted into classified dollars per hundredweight values assuming a 3.5% butterfat content shown below. Note an across-the-board, near-dollar-per-hundredweight increase in the make allowance suggested under the new study. Since make allowances are used in the end-product pricing formulas for Class I and II milk, values used in the calculation of Class III and IV milk, make allowances effectively reduce the regulated value of milk in all classes.

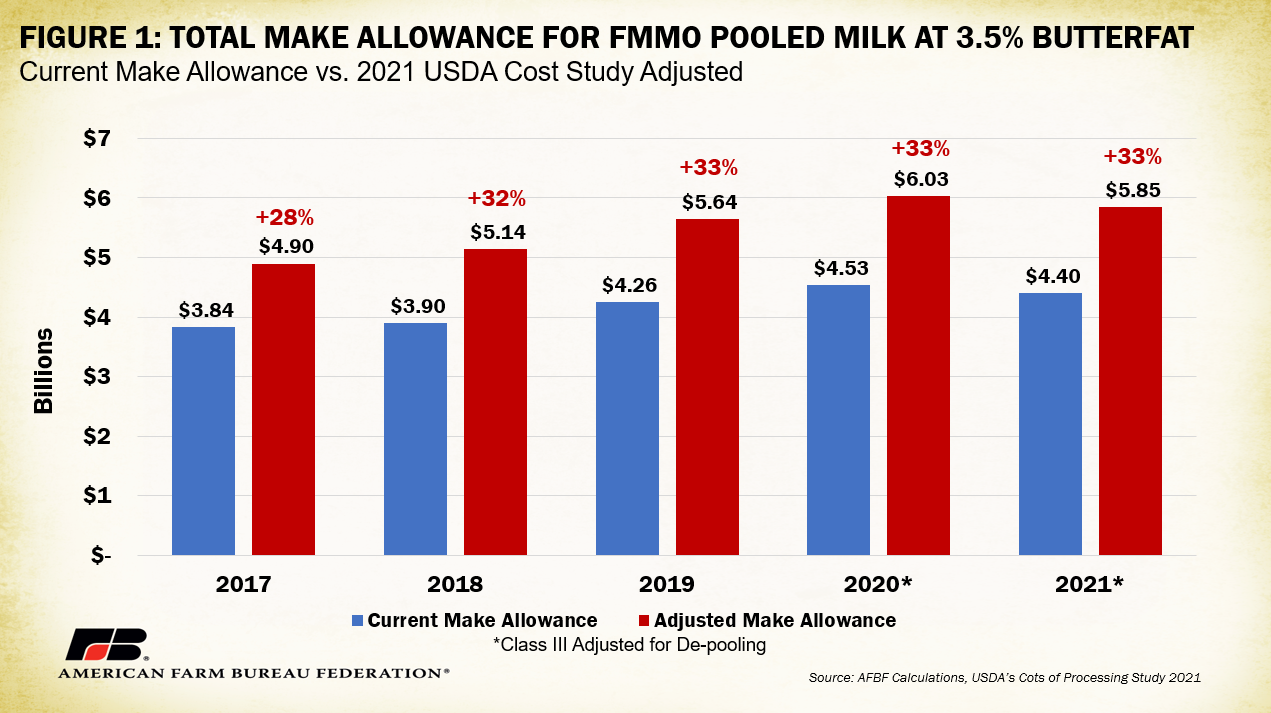

Combining data from USDA’s Agricultural Marketing Service on total class utilization volumes with the classified value make allowances indicate total make allowances – based on 3.5% butterfat content – would have increased nearly 33% under these updated cost study results values in 2021. This equates to a single-year $1.45 billion FMMO-wide increase in milk formula deductions to cover estimated increases in processor costs. Figure 1 displays annual cumulative values of make allowances from 2017 to 2021 under the current value system and the adjusted values based on the cost study. Across these five years, the adjusted values would have increased total make allowances by $6.6 billion, reducing the regulated revenue dairy farmers would have received for their milk by the same magnitude, all else held equal. Note that 2020 and 2021 Class III pooling values are adjusted to account for de-pooling prompted by COVID-19 market forces.

Conclusion

USDA’s 2021 Cost of Processing in Cheese, Whey, Butter and Nonfat Dry Milk Plants study suggests processing costs to transform fluid milk into manufactured dairy products have increased for cheese, nonfat dry milk and whey from both the 2006 estimations and currently enforced make allowances. This was an expected result given lingering supply chain disruptions that have heightened input and labor costs across the broader economy. Any process to change make allowances to reflect higher processing costs will consider additional input and information when determining new values. This means the study will likely not be the sole determinant in future make allowance changes. Any increase in make allowances can lower the price of milk dairy farmers receive, reducing already shrunken margins, but must be balanced against the need to maintain sufficient plant capacity to process milk. Careful consideration of the widespread impact make allowance alterations have on dairy farmers’ bottom lines is essential to any effort, by hearing or statute, to change them.