The Impact of Irma on Florida Oranges Likely to Get Worse

TOPICS

Weather

photo credit: Florida Farm Bureau, Used with Permission

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

Florida is home to hundreds of agricultural products from blueberries and strawberries to tropical fish, sugar, milk, cheese and - most notably - oranges. However, for nearly two decades Florida’s flagship product has been dealing with a number of challenges.

First, per capita consumption of orange juice has declined by nearly 50 percent to less than 3 gallons per person. Over this same time, imports as a share of total orange juice consumption has surged to nearly 50 percent. Then, beginning in 2005, Florida orange growers have been fighting a devastating pathogen that causes citrus greening disease. Citrus greening ultimately results in irregularities in the size and color of the orange and causes a bitter flavor. Since 2005, when the disease first reached Florida, and combined with these other challenges, orange utilization (i.e. production) has declined by more than 50 percent.

Now, on the back of Hurricane Irma in early September, the 2018 Florida orange crop is projected by USDA to be the smallest in more than 70 years, down more than 20 percent from the 2017 crop size, at 54 million boxes. Florida represents more than 50 percent of total U.S. orange utilization, and as a result, total U.S. orange utilization is projected to be down 16 percent from 2017 at 101.7 million boxes.

USDA Orange Crop Projections

On the ground reports following Hurricane Irma indicated that citrus groves had been devastated with uprooted trees, flooding and fruit knocked to the ground. It was estimated that as much as 80 percent of the production in south Florida was lost and nearly 100 percent of the orange production in southwest Florida was lost in the storm. A recent Florida Citrus Mutual’s grower damage survey estimated the crop at closer to just 31 million boxes, 23 million boxes below USDA’s October estimate. Based on these reports, the market was anticipating a steep drop in the size of the orange crop for 2018.

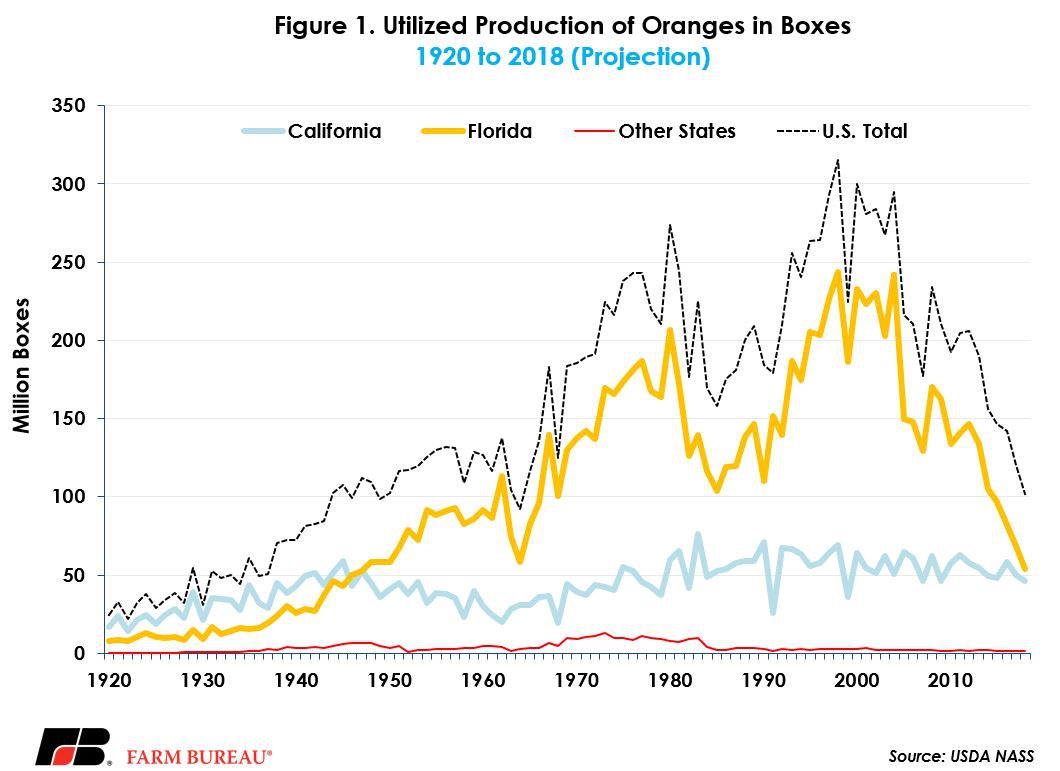

USDA (partially) confirmed expectations of a smaller orange crop in Florida. USDA’s Oct. 12 Crop Production report provided the first objective yield survey estimate for the size of the 2018 orange crop. U.S. orange utilization was projected at 4.34 million tons (101.7 million boxes), down 16 percent from the prior year’s utilization, Figure 1.

Florida orange utilization was projected at 2.43 million tons (54 million boxes at 90 pounds per box), down 21 percent from the prior season. Hit hardest was Florida’s early, midseason, and navel varieties. Utilization of these oranges was projected at 1.04 million tons, down 30 percent from last season. Finally, Florida Valencia orange utilization was projected at 1.40 million tons, down 13 percent from last season.

California is the nation’s second-largest producer of oranges. California orange utilization was projected at 1.84 million tons (46 million boxes at 80 pounds per box), down 9 percent from last year. California navel orange utilization for 2018 was projected at 1.40 million tons, down 11 percent from the prior year. California Valencia orange utilization was unchanged from last year at 440,000 tons.

Production in Texas, approximately 2 percent of the U.S. crop, was projected at 70,000 tons (1.65 million boxes at 85 pounds per box), up 20 percent from last season.

While USDA confirmed a smaller orange crop, many in the trade believe the crop production estimate does not reflect the damage from Hurricane Irma as of yet. Many now expect that next month’s projection will be a more realistic estimate. Consider this assessment from Florida Farm Bureau Federation:

Our members have experienced additional fruit drop in the weeks since the storm due to the wind damage their trees sustained during the storm.

Jaime Jerrels, Director of Agricultural Policy, Florida Farm Bureau Federation

How Small Could the Florida Orange Crop Get?

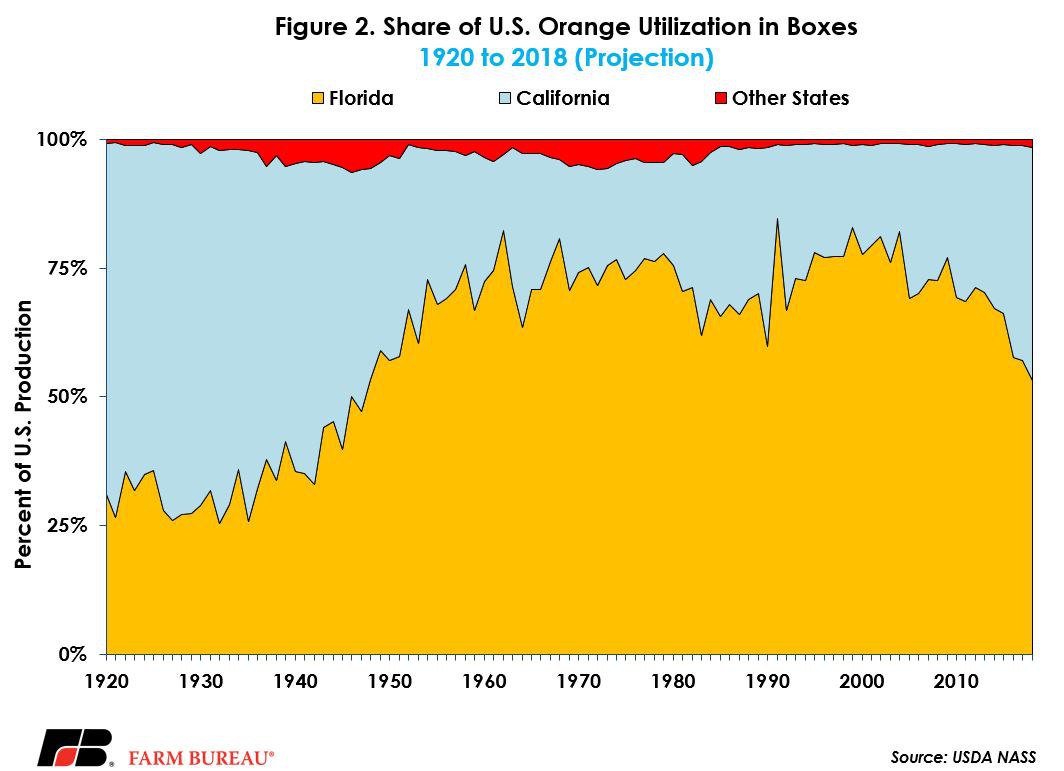

Since 1946 Florida has been the nation’s leader in orange utilization, reaching a high of 83 percent of the total U.S. utilization in 1999, Figure 2. However, for nearly the last decade, Florida’s market share has been declining. Florida’s 2018 market share is now projected at 53 percent, slightly higher than California’s 45 percent market share. The difference between California and Florida orange utilization is as narrow as it has been in more than 70 years. If Florida orange utilization falls by 590,000 tons or 8 million boxes, a likely possibility some say, Florida would have a smaller market share than California for the first time since the 1944-1945 season.

The objective yield survey for the Oct. 1 forecast was conducted in Florida during August and September. The USDA procedures that were used in this projection are the same as in past seasons. However, Hurricane Irma made landfall shortly after Labor Day and eventually dissipated by mid-September. Thus, a portion of USDA’s survey of the number of bearing trees and the number of fruit per tree could potentially have occurred pre-hurricane. USDA indicated as much, stating that the storm came just as they were finishing up their limb counts.

In the upcoming months USDA will conduct fruit size measurement and fruit droppage surveys to update the orange production forecast. A new production forecast will be released monthly throughout the growing season, so these numbers are very likely to change as new information is received by USDA. Events like freezes or hurricanes are why orange crop estimates are updated monthly throughout the season. Many believe the timing of Hurricane Irma was just out of sync with the count to be included in the most recent projection.

While the market was surprised by USDA’s orange utilization estimate, resulting in a 3 percent drop in frozen orange juice futures, plenty of uncertainty remains. USDA will revise the production forecast in the Nov. 9 Crop Production report. At that point, the impact of Hurricane Irma will be more fully revealed and will most likely result in USDA reducing the size of the orange crop. While all eyes will be on this next report, any production declines in the U.S. are more than offset by the significantly larger Brazilian crop – currently projected at 19.2 million metric tons – and as a result, upside price potential may be limited.