September WASDE Drops Corn, Soybean Production, Increases Cotton Production; Wheat Unchanged

TOPICS

Wheat

photo credit: Arkansas Farm Bureau, used with permission.

Bernt Nelson

Economist

USDA Production Estimates Adjust Downward After Objective Yield Plot Data is Collected

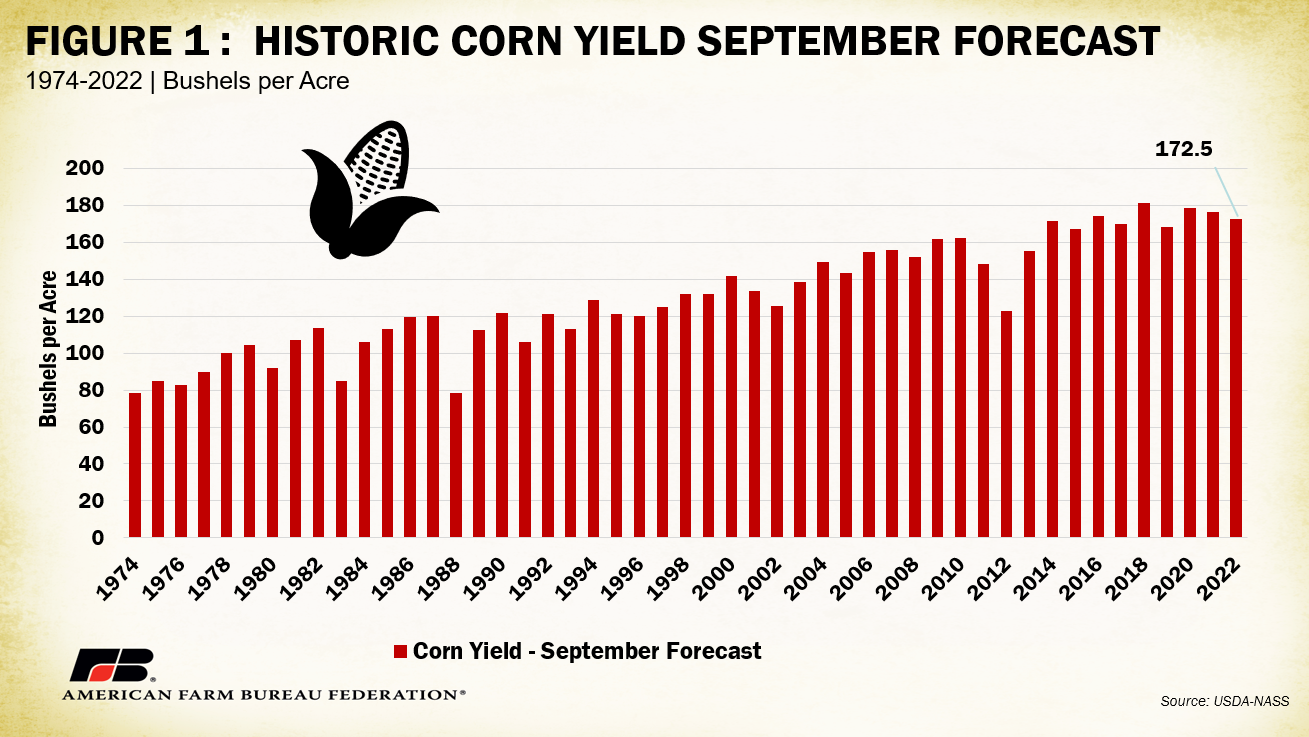

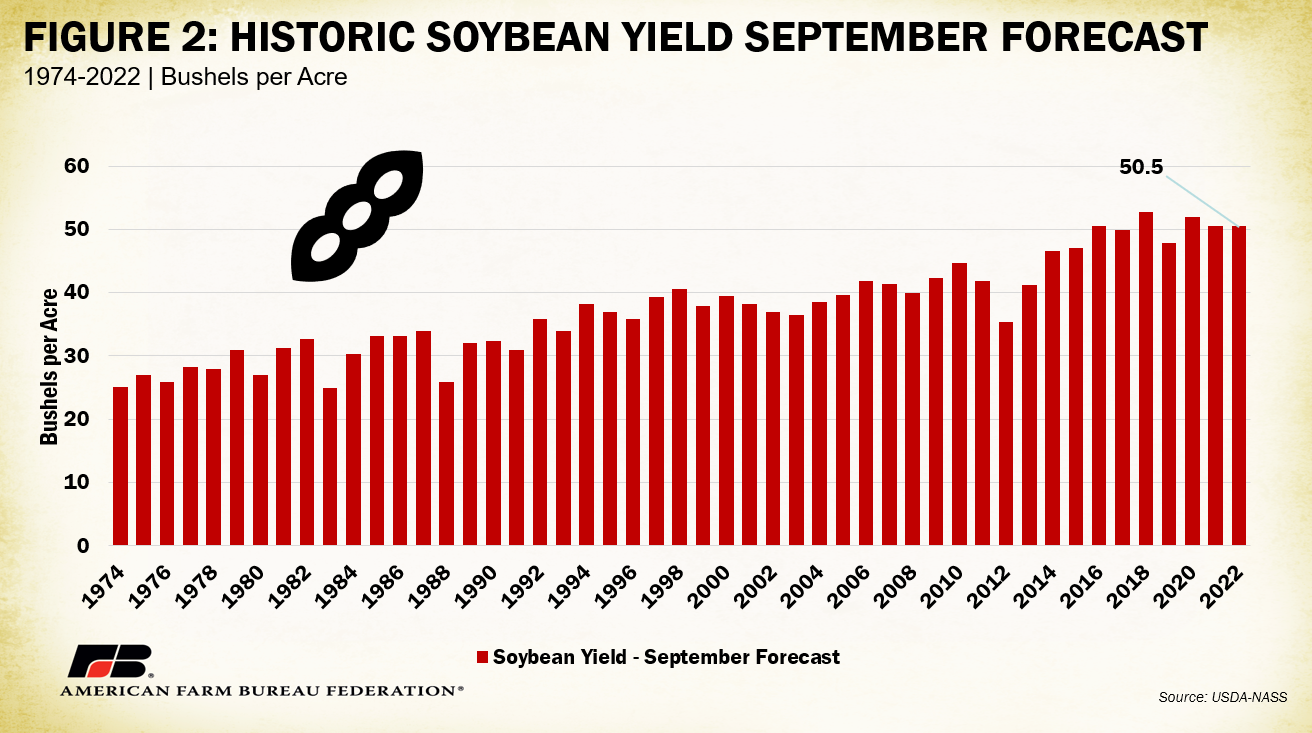

The monthly World Agricultural Supply and Demand Estimates, released Monday by USDA’s Office of the Chief Economist, decreased corn supply for the start of the new marketing year, largely driven by a drop in production from a reduction in national average yield and area harvested. Corn production is forecast 415 million bushels lower than last month at 13.9 billion bushels. The national yield for corn is forecast at 172.5 bushels per acre, down 2.9 bushels or 2% from last month. USDA increased soybean beginning stocks and decreased production. The higher beginning stock numbers reflect a smaller export forecast for 2021/22. Soybean production was forecast down 152 million bushels at 4.4 billion due to smaller harvested area and yield. Harvested area is down 0.6 million acres from August. Soybean yield is forecast at 50.5 bushels per acre, down 1.4 bushels or 3% from last month. USDA increased 2022/23 cotton production and ending stocks compared to August. Production was forecast at 13.8 million bales, 1.3 million bales higher than August due to higher production expectations in most major cotton-producing states despite the slight decrease in average yield. The 2022/23 wheat outlook for September is unchanged.

Corn

For the close of the 2021/22 corn marketing year, a decrease of 50 million bushels in ethanol use and a decrease of 25 million bushels in corn exports decreased USDA’s ending stocks estimate to 1.22 billion bushels, down 12% from the August estimate of 1.39 billion bushels. USDA estimates the 2022/23 marketing year price at $6.75 per bushel, up 10 cents compared to August and up 80 cents compared to 2021. The stocks-to-use ratio of 8.5% is down 1.8% from 2021 and up only slightly from the 10-year low of 8.3% in 2020.

For the new 2022/23 corn marketing year that started Sept. 1, USDA indicates that corn farmers planted 900,000 fewer acres of corn than reported in the June 30 Acreage report, moving corn area planted to 88.6 million acres, down 5% compared to 2021. This estimate, in conjunction with a decrease in yield from 175.4 bushels per acre reported in the August Crop Production Survey report to 172.5 bushels per acre, a 2.5% decrease compared to 2021 – decreases corn production for the year from 14.75 billion bushels to just over 13.9 billion bushels. This is almost 4% lower than what USDA anticipated production to be when estimates were first reported in May and is 7.7% below corn production in 2021. With the corn carry-over quantity decreased as well, USDA reported the corn supply at 15.49 billion bushels, down 5.4% compared to 2021.

For corn demand, USDA dropped total use by 250 million bushels. Additionally, USDA decreased the feed and residual use category by 100 million bushels, from 5.33 billion bushels to 5.23 billion bushels, down 6.7% compared to 2021, and left corn exports unchanged at 2.27 billion bushels, down just over 7% from 2021 levels. For 2022/23, ethanol use is on track with just under a 1% decrease at 5.33 billion bushels compared to 2021/22 when ethanol use was 5.38 billion bushels. Adjustments made to supply and demand this month caused ending stocks to drop 169 million bushels, from 1.39 billion bushels to 1.22 billion bushels, down 12% compared to 2021 ending stocks. This also pressured the 2022/23 marketing year average farm price for corn higher from $6.65 per bushel last month to $6.75 per bushel – 80 cents per bushel above the corn price for the 2021/22 marketing year.

Soybeans

At the close of the 2021/22 marketing year, USDA lowered soybean crushing by 20 million bushels to 2.2 billion bushels and lowered export estimates for soybeans by 70 million bushels to 2.09 billion bushels. The stocks-to-use ratio dropped from 5.4% to 4.5%, however, the average farm price for soybeans for the 2022/23 marketing year was unchanged at $14.35 per bushel, an 8% increase compared to 2021.

The new soybean marketing year for 2022/23 started Sept. 1 and USDA estimates indicate soybean farmers decreased planted acres by 3.5 million compared to the June Acreage report. This means that soybean planted area moved from 91 million acres to 87.5 million acres, which is just under a 2% increase compared to the 86.3 million acres planted in 2020. USDA dropped soybean yield to 50.5 bushels per acre compared to the 51.9 bushels per acre reported last month in the August Crop Production Survey and 1.5 bushels below early estimates in May that soybean yields would be 51.5 bushels per acre. Soybean yields at this level are 1.7% below the 2021 record of 51.4 bushels per acre. The yield drop decrease resulted in a soybean production estimate of 4.38 billion bushels, down 1.3% compared to 2021.

Soybean demand estimates for 2022 were revised in September compared to August as USDA lowered soybean crushing use by 20 million bushels to 2.23 billion bushels, nearly 1% higher than 2021 crushing, and decreased soybean exports by 70 million bushels from 2.16 billion bushels to 2.09 billion bushels. However, soybean exports are on track to be about 3% behind the 2.16 billion bushels of exports in 2021. Adjustments made to supply and demand in this month’s report dropped ending stocks from 245 million bushels to 200 million bushels, which is 11% lower than ending stocks reported for 2021. The 2021/22 marketing year average price for soybeans is $14.35 per bushel, unchanged from last month, but $1.05 per bushel above the 2021/22 marketing year average price.

Wheat

Wheat planted acreage has changed only slightly across the 2022/23 marketing year at 47 million acres, less than 1% below the number of acres planted in 2021. Yields this month remained unchanged compared to the August estimate at 37.5 bushels per acre. This is also unchanged from earlier estimates in the year of 37.5 bushels per acre, and nearly unchanged compared to 2021 when farmers reported 37.2 bushels per acre. Wheat production in 2022 is estimated by USDA to be 1.78 billion bushels, about 8% ahead of 2021 when production reached 1.65 billion bushels. USDA made no revisions for use. USDA estimates total U.S. wheat supply at 2.53 billion bushels in 2022, which is 1.3% behind the 2021 supply of 2.59 billion bushels and 14% behind the 2020 supply of 2.9 billion bushels.

On the demand side for the 2022/23 marketing year, food use for wheat is up 6 million bushels from 964 million bushels in 2021 to 970 million bushels in 2022. Seed use is up 8 million bushels from 2021 levels, at 68 million bushels. Wheat exports from the U.S. are about 3% ahead of 2021 levels, with 825 million bushels expected to be exported in the 2022/23 marketing year compared to 800 million bushels exported in the 2021/22 marketing year. USDA estimated ending stocks at 610 million bushels – 8% lower than in 2021 when ending stocks were 615 million bushels. The stocks-to-use ratio for wheat in 2022/23 currently sits at 31.4%, which is 2.9% lower than in 2021/22. USDA estimates the average farm price for wheat in 2022/23 is $9.00 per bushel, down $1.75 from initial estimates for the marketing year early this spring and up $1.37 per bushel compared to 2021.

Cotton

The 2022/23 marketing year for cotton began on Aug. 1. For the September WASDE, USDA revised cotton area planted up from 12.48 million acres in August to 13.79 million acres, which is almost 19% higher than the 11.22 million acres planted in 2021. With the revised 2022/23 yield decrease from 846 pounds per acre in August to 843 pounds per acre (3.3% higher than y2021 yields) USDA estimates cotton production to reach 13.83 million 480-pound bales, a decrease of 21% compared to 2021 when production reached 17.52 million 480-pound bales, and up from last month’s estimate by 10%. With carry-over stocks of 3.75 million 480-pound bales, cotton supply in 2022/23 is on track to reach 17.59 million 480-pound bales, about 15% below total supply in 2021.

On the demand side for cotton, domestic use remained unchanged from August at 2.3 million 480-pound bales, a decrease of 10% compared to 2021. However, estimates for cotton exports increased by 600,000 480-pound bales from August to September, now registering 12.6 million 480-pound bales, about 14% lower than exports in 2021 when 14.62 million 480-pound bales were exported. The adjustments made in supply and demand pressured ending stocks upward from 1.8 million 480-pound bales in August to 2.7 million 480-pound bales, which is 28% lower than in 2021. The stocks-to use ratio for the 2022/23 marketing year sits at 18.1%, down 2.2% compared to 2021. The average farm price for cotton decreased 1 cent per pound from August to September and now sits at 96 cents per pound, up 4% from the 2021/22 marketing year price.

Summary

In its September WASDE, USDA applied its objective yield plot results to crop production estimates, resulting in decreased yield estimates for corn, soybeans and cotton for the 2022/23 marketing year, while leaving wheat unchanged. USDA estimated corn production down 3.6%, soybean production down 1.3% and cotton production down 21% compared to 2021 levels. Meanwhile, wheat production is up almost 8% compared to 2021.

The supply changes have resulted in tighter margins especially in corn, soybeans and wheat while cotton saw slight increases. Ending stocks for corn and soybeans decreased in September estimates compared to August while wheat was unchanged and cotton saw increases. The biggest surprise for this report was the decrease in soybean ending stocks, largely due to a 3% drop in yield. Corn ending stocks were also affected by a 4.5% decrease in yields from 175.4 bushels per acre to 172.5 bushels per acre. These adjustments should provide some support for higher prices for corn and soybeans for a strong start to the new marketing year that began Sept. 1.