October Cattle on Feed Report Shows Placements, Marketings, Inventory Up

TOPICS

USDAMichael Nepveux

Economist

photo credit: Colorado Farm Bureau, Used with Permission

Michael Nepveux

Economist

USDA’s latest Cattle on Feed report, released October 23, shows the number of animals on feed as of October 1 is higher than it was this time last year. The report provides monthly estimates of the number of cattle being fed for slaughter. For the report, USDA surveys feedlots of 1,000 head or more, as this represents 85% of all fed cattle. Cattle feeders provide data on inventory, placements, marketings and other disappearance.

October Cattle on Feed Report

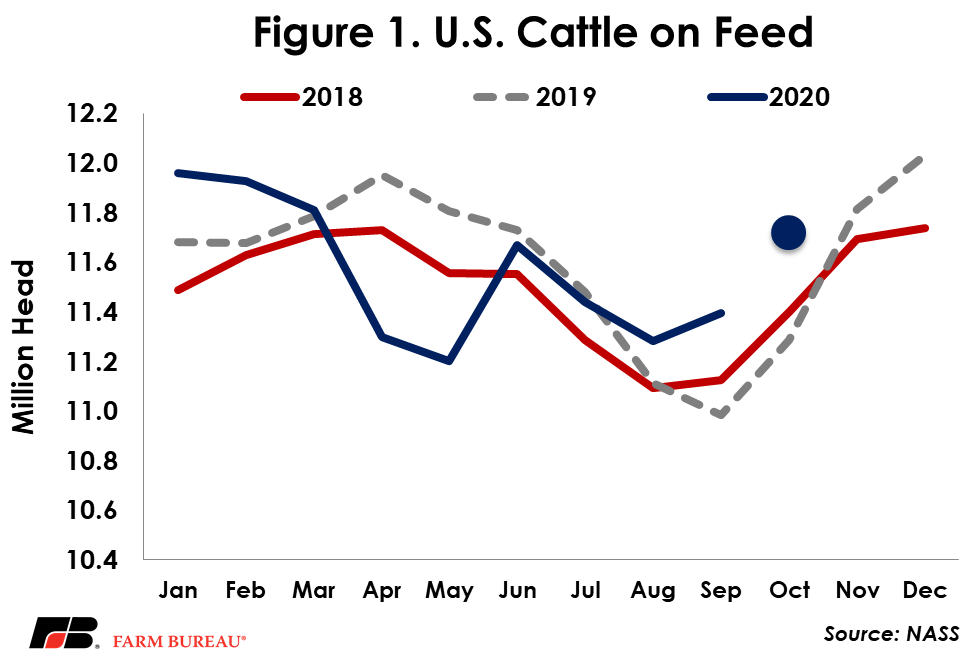

This report showed a total inventory of 11.717 million head for the United States on October 1, the highest October 1 inventory level since the series began in 1996. This 3.8% year-over-year increase is slightly above analysts’ expectations of an average increase of 3.2% in feedlot inventories. Large placements helped to offset the large marketings and pushed cattle on feed up 429,000 head over last year. Typically, October begins the slow build up of animals after September lows, and this year it looks as if we are seeing this seasonality play out. After strong impacts from the pandemic in April and May, the number of cattle on feed has largely followed seasonal patterns.

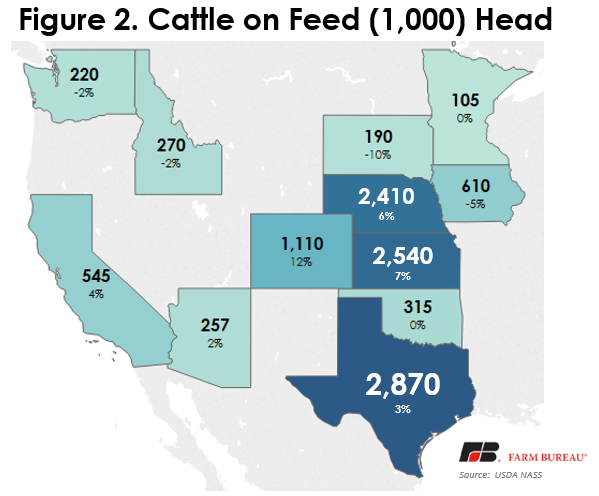

As usual, Texas, Kansas and Nebraska lead the way in total fed cattle numbers, accounting for nearly 7.6 million head, or approximately 65% of the total on-feed inventory in the country. Texas continued to gain year-over-year, adding 3% relative to 2019. Kansas and Nebraska saw greater gains, adding 7% and 6% respectively.

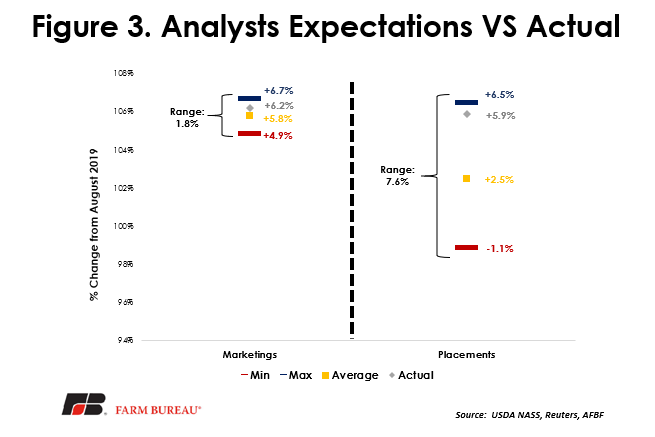

While total inventories are an important component of the report, other key factors include placements (new animals being placed on feed) and marketings (animals being taken off feed and sold for slaughter). Coming in at 5.9% over 2019, placements in September far exceeded the average analyst expectation of a 2.5% increase and were relatively close to the maximum analyst expectation of a 6.5% increase. The relatively wide range of forecasts for placements – nearly 8% -- somewhat highlights the uncertainty that still exists in the market around the full impacts of COVID-19. Placements clocked in at 2.227 million head in September. Marketings came in at 6.2% above last year. This is slightly above analysts’ expectations of 5.8% above year-ago levels. The 1.846 million head that were marketed in September marks the highest level for that month in nearly two decades.

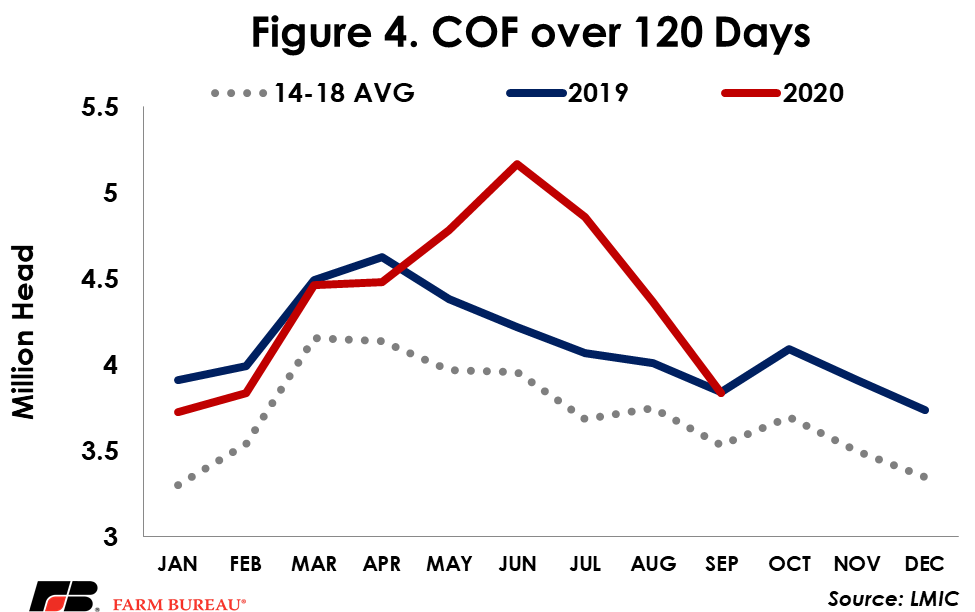

In September, the industry continued working through the backlog of heavier animals in the system. Figure 4 shows we are back in line with previous years’ numbers of estimated animals on feed over 120 days, and many in the industry believe that we have largely worked our way through that backlog.

Summary

With plenty of animals in the pipeline for processing, the October Cattle on Feed report is considered relatively bearish. However, the impacts of the pandemic are still reverberating throughout the economy, contributing to market uncertainty. It will be interesting to see how the recession eventually impacts beef demand, as recessions tend to not be kind to this particular animal protein.

Trending Topics

VIEW ALL