First Look at 2021/22 Marketing Year Following Sky-Rocketing 2020/21 Export Demand

TOPICS

Wheat

photo credit: Right Eye Digital, Used with Permission

Shelby Myers

Economist

The May World Agricultural Supply and Demand Estimates gives the first look at the newest marketing year demand expectations since the USDA Agricultural Outlook Forum in February. This is the highlight of spring USDA reports as it incorporates farmer planting decisions from the March Prospective Planting report and adapts supply estimates to reflect weekly planting progress reports. The big story leading up to this report is rising prices due to the increased global demand for U.S. commodities. This Market Intel dives into the May WASDE for updated estimates of the current 2020/21 marketing year crop and assesses what could be in store for the newest 2021/22 marketing year, which starts in September.

Corn

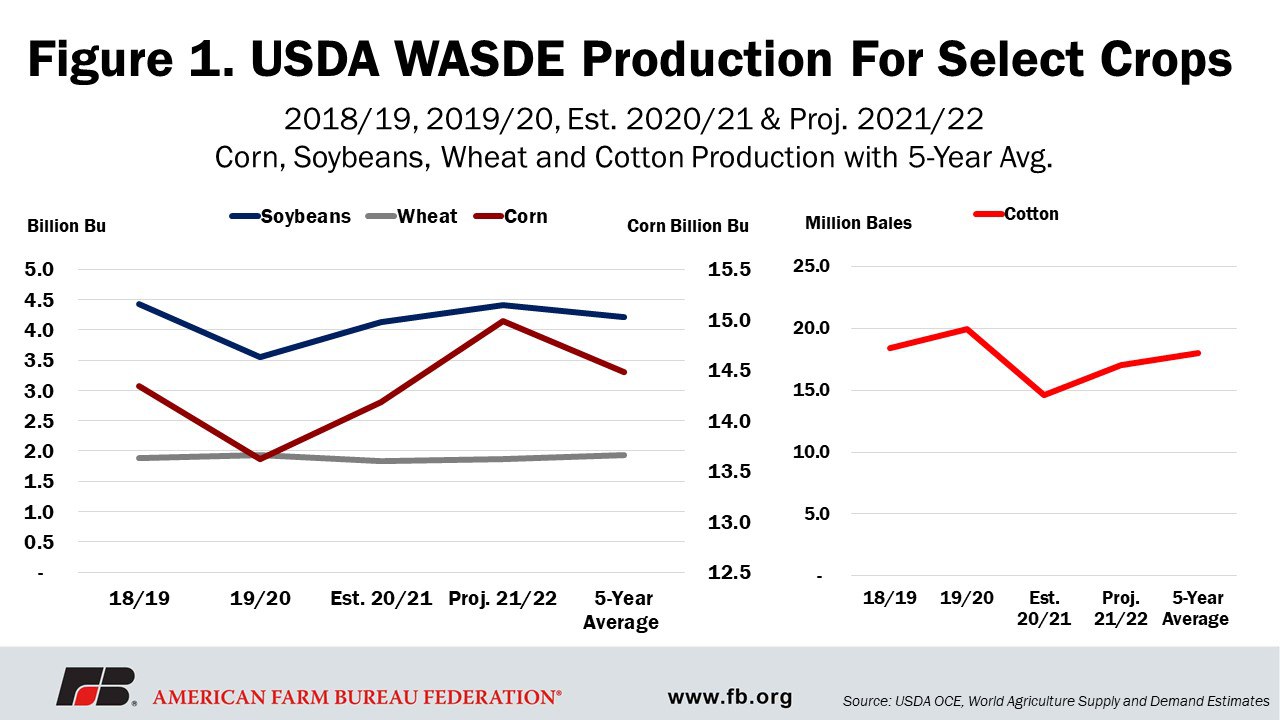

USDA estimates corn planted for the 2021/2022 marketing year at 91.1 million acres, just slightly up from 2020, when 90.8 million acres of corn were planted. USDA forecasts farmers will harvest 83.5 million acres of corn in 2021 at a yield rate of 179.5 bushels per acre. At these estimates, corn production for 2021/2022 is estimated to be slightly under 15 billion bushels, just behind 2016’s 15.1 billion bushels. Keep in mind, the production estimate for the 2021 level is a 6% increase from 2020, when U.S. farmers produced just over 14.1 billion bushels, and a 4% increase from the five-year average of 14.4 billion bushels.

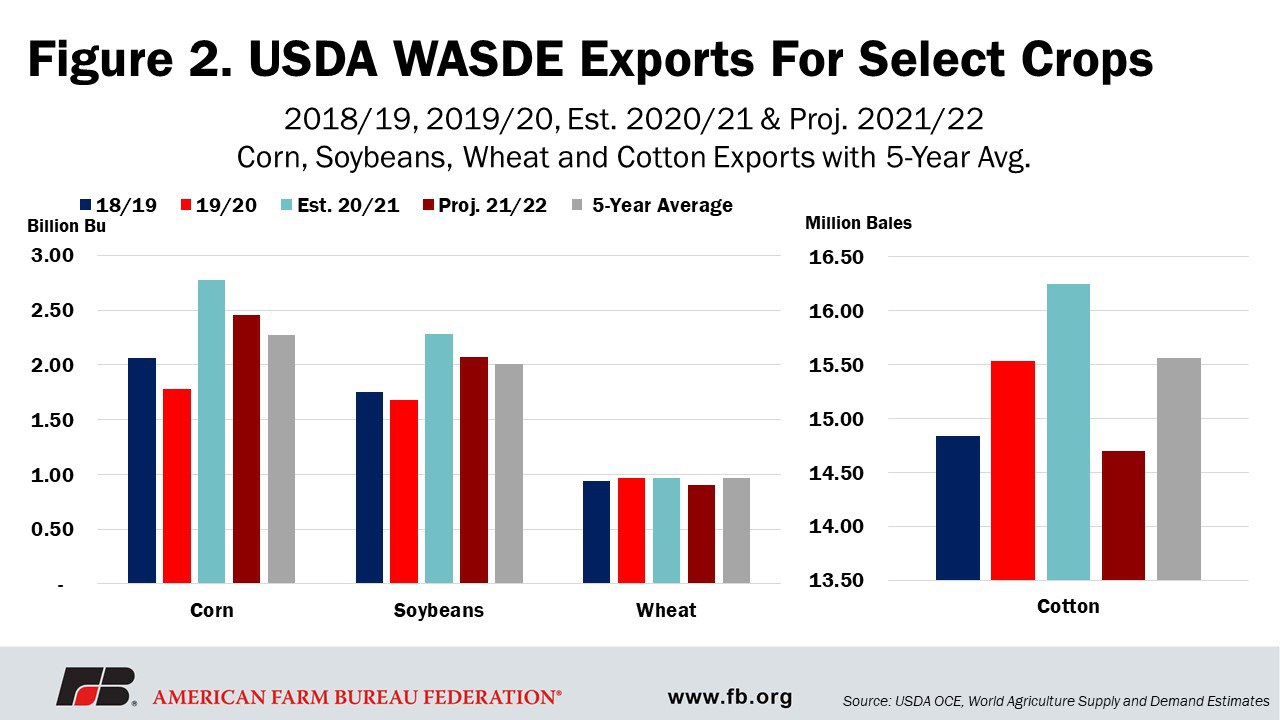

On the demand side, for the new 2021/22 marketing year, USDA estimates ethanol use will rebound, increasing by 225 million bushels, or 4.5%, from the 2020/21 marketing year. This rebound is largely driving the overall increase in domestic corn use expected for the newest marketing year. Corn export estimates for the newest marketing year seem to be unexciting considering the most recent surge to exports in the current marketing year. USDA estimates peg 2021/22 exports at 2.45 billion bushels, down 12% from where exports are currently tracking in the 2020/21 marketing year.

This month, USDA estimates 2020/21 corn exports to be a record 2.7 billion bushels. At this time last year, the agency had anticipated exports to only be 2.15 billion bushels, but the pace of exports and increased global buying has boosted estimated exports by 29% in just a year.

All this being said, for marketing year 2021/22 estimates, the uptick in ethanol and decrease in exports pushes USDA’s estimate for corn ending stocks just above 1.5 billion bushels. When compared to the current marketing year, ending stocks have fallen to 1.2 billion bushels, down 62% from the 3.3 billion bushels first reported for the 2020/21 marketing year this time last year. These early demand expectations have a lot of room to change over the course of the coming months.

USDA estimates put the 2021/22 stocks-to-use ratio at 10.2%. When looking at the current 2020/21 marketing year, the corn stocks-to-use ratio has fallen to its lowest level since 2012 at 8.5%. For the 2021/22 corn price, USDA puts corn at $5.70 per bushel, while the 2020/21 marketing year price increased to $4.35 per bushel from $4.30 last month.

Soybeans

Soybean farmers are expected to plant 87.6 million acres of soybeans in 2021/2022, up 5.4% from 2020, when farmers planted 83.1 million acres. Looking back to 2019, soybean farmers only planted 76.1 million acres, down 15.1% compared to estimates for the upcoming marketing year. As part of soybean supply expectations for 2021/22, soybean yields are at 50.8 bushels per acre, with 86.7 million harvested soybean acres. Compared to 2020 when soybean production was 4.1 billion bushels, U.S. farmers are expected to produce 4.4 billion bushels of soybeans in 2021, an increase of 7% and an increase of 5%, compared to the 5-year average.

The increase in soybean supply for 2021 follows heightened soybean demand in 2020, largely driven by exports. While 2020/21 marketing year soybean exports are at 2.28 billion bushels, it’s an increase of 11% from when 2020/21 soybean exports were first estimated to be just over 2 billion bushels in May 2020. Demand expectations for the 2021/22 marketing year are slightly lower, with 205 million fewer bushels of soybeans anticipated to be exported.

For the newest marketing year, the expected production increase is offset by lowered export expectations, but ending stocks are expected to be relatively close to 2020/21 ending stocks. For 2021/22, soybean ending stocks are estimated at 140 million bushels, while the 2020/21 ending stocks are currently estimated to be 120 million bushels. Comparing the stocks-to-use ratio, the 2021/22 marketing year is slightly higher at 3.2% compared to 2020/21 for which the U.S. is on pace for a 2.6% soybean stocks-to-use ratio matching the lowest stocks-to-use ratio in 2013.

For both years, the expected continuation of lower soybean stocks is pushing prices higher. For the 2020/21 marketing year, the average farm price for soybeans remains at $11.25 per bushel, where it was last month. The 2021/22 marketing year average farm price is estimated to increase 23% to $13.85 per bushel.

Figure 1 displays U.S. crop production for corn, soybeans, wheat and cotton since the 2018/19 marketing year, including the new 2021/2022 projections and the five-year average.

Wheat

Wheat planted acres in 2021/2022 are estimated at 46.4 million acres, an increase of 4.7% from 2020/21’s 44.3 million acres. Yield is estimated to be 50 bushels per acre, leading wheat production to potentially reach well above 1.872 billion bushels, a 2.5% increase from 2020/2021 wheat production, which reached 1.826 billion bushels. While wheat production has increased in the past two years, it still sits about 3% below the five-year average of 1.938 billion bushels.

Wheat demand in 2020/2021 increased from earlier-in-the-year expectations but sat almost parallel to demand in 2019/20. For the newest marketing year, wheat is expected to be a livestock feed substitute and the feed-use category is largely driving the overall wheat-use estimate. Feed use of wheat for 2021/22 is expected to increase by 70 million bushels from 2020/21, while exports for the newest marketing year are anticipated to pull back 65 million bushels.

The anticipated increase in production helps supply meet some of the crop demand, however, increased domestic uses for wheat in the newest marketing year are expected to lead to lower ending stocks. 2021/22 ending stocks for wheat are estimated at 774 million bushels, a decrease of 1% from the 872 million bushels of ending stocks in 2020/21. The resulting stocks-to-use ratio for wheat in 2021/22 is expected at 37%, its lowest level since 2014, while 2020/21 stocks-to-use sits just above 41%.

USDA estimates the average farm price of wheat for the 2020/21 marketing year to be $5.05 per bushel, a 9% increase from estimates this time last year, when USDA expected the crop price to be $4.60 per bushel. Into the newest marketing year, USDA estimates the 2021/22 marketing year average price of wheat to be $6.50 per bushel, the first time it would be above $6 since 2013.

Cotton

Cotton planting expectations for the 2021/2022 marketing year are 12.04 million acres, which is very close to 2020/21’s 12.09 million acres. USDA does not anticipate a yield bump for the new marketing year and expects the 847 pounds per acre of 2020 to be matched in 2021. However, farmers are expected to harvest 9.63 million acres of cotton in 2021, a 16% increase from the 8.28 million acres harvested in 2020. This anticipated increase in cotton harvest is expected to bump 2021 cotton production to 17 million bales, up from the 14.6 million bales produced in 2020. Despite the increase, this is about 6% below the five-year average of 18 million bales of cotton produced in the U.S.

Demand for cotton in the 2020/21 marketing year, particularly exports, has helped decrease the accumulated ending stocks of the crop from previous years. With lower-than-expected supply in 2020 and the continued increase in exports -- now sitting at 16.25 million bales, up from 15 million bales estimated this time last year -- overall cotton use in 2020/21 is at its highest since 2017. For the newest marketing year, coming in with less carry-over helps offset increased production expectations that can be helpful with a reduction in expected exports. In the 2021/22 marketing year, USDA expects cotton exports to decrease to 14.7 million bales, down 9.5% compared to 2020/21.

2020/2021 cotton ending stocks are pegged at 3.3 million bales and USDA estimates that the production increase and export decrease will lead to similar ending stock estimates for the 2021/22 marketing year at 3.1 million bales. For 2020/21, USDA estimates have the cotton stocks-to-use ratio sitting at 17.8% and the 2021/22 stocks-to-use ratio slightly higher at 18%. If the 2021/22 stocks-to-use ratio comes to fruition, it would sit about 27% lower than the five-year average, which is typically around 24.5%.

The decrease in stocks relieves a heavy weight that has been sitting on cotton prices for the past few years. For the 2020/2021 average marketing year price, USDA estimates cotton at 68 cents per pound, up 11 cents per pound from this time last year. For the 2021/22 marketing year, USDA expects the cotton price to reach 75 cents per pound, its highest price since 2013.

Figure 2 displays the U.S. exports for corn, soybeans, wheat and cotton since the 2018/19 marketing year, including the new 2021/2022 projections and the five-year average.

Summary

The May WASDE is the long-awaited first look at the upcoming marketing year for corn, soybeans, wheat and cotton. There is a lot of room for changes over the coming months. This May WASDE comes on the heels of massive export increases that helped boost prices for all four crops. Farmer planting decisions will not be updated until the June 30 acreage report, providing a better idea of supply expectations for the newest marketing year. Given the sharp increase in prices for corn and soybeans, changed planting intentions could result in revised supply expectations for the 2021/2022 marketing year early on. Additionally, demand changes like those that occurred late into calendar year 2020 could change the outlook of crop expectations finishing 2020/21 and heading into 2021/22.

Top Issues

VIEW ALL