First Glimpse at 2021 Acreage and Yields

TOPICS

Wheat

photo credit: AFBF Photo, Philip Gerlach

John Newton, Ph.D.

Former AFBF Economist

Every November, USDA releases a 10-year baseline projection including long-term supply, use and price projections for major U.S. crops and livestock products. These supply and demand projections come in advance of the department’s annual Agricultural Outlook Conference during which commodity supply and use projections, projections for farm income and expectations for global commodity trade are reviewed. Today’s article reviews planted acreage and yield expectations from the recently released USDA Agricultural Projections to 2030 report for the 2021/22 crop year for corn, soybeans and wheat.

Background

Building on the October World Agricultural Supply and Demand Estimates, USDA’s long-term agricultural projections represent the department’s consensus projections for U.S. supply and demand for major crop and livestock sectors over the next 10 years. The projections are based on economic models and judgment-based analyses. Importantly, these baseline projections do not represent official USDA forecasts, but rather reflect a long-run outlook based upon specific assumptions about macroeconomic conditions, policy, weather and international developments given current policies, e.g., the 2018 farm bill or the Phase 1 agreement with China. This baseline projection does not include external weather or policy shocks, so in other words, it assumes business as usual for U.S. commodity markets.

Acreage Expectations for 2021/22

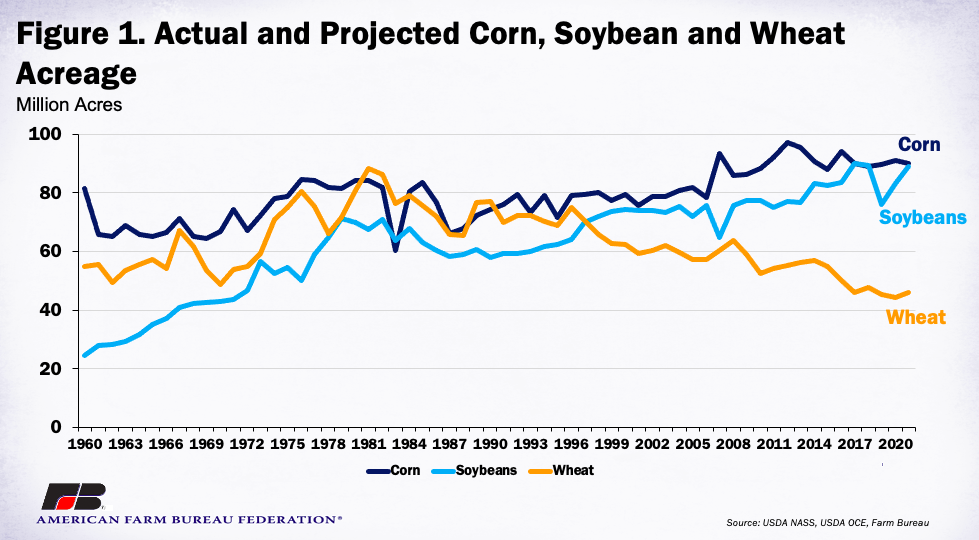

On the back of strong export demand, lower ending stocks and higher prices, USDA projects soybean acreage will increase by nearly 6 million acres, or 7%, from 2020 to 89 million acres planted. If realized, 2021 soybean acreage would be the third-highest acreage on record, behind only 2017 and 2018.

Despite higher corn prices in recent weeks and current expectations for shrinking stockpiles, USDA projects corn acreage for 2021 will decline by 1 million acres, or 1.1%, from 2020. If realized, total corn and soybean planted area would be 179 million acres, the second-highest acreage on record, behind only 2017 when more than 180 million acres were planted.

During 2020, all wheat planted acreage was 44.3 million acres, the lowest wheat acreage on record. Headed into the 2021/22 marketing year with a lower wheat inventory and higher expected prices, USDA projects wheat acreage will increase by more than 1.6 million acres, or nearly 4%, to 46 million acres. Figure 1 highlights actual and projected acreage for soybean, corn and wheat.

Yield Expectations for 2021/22

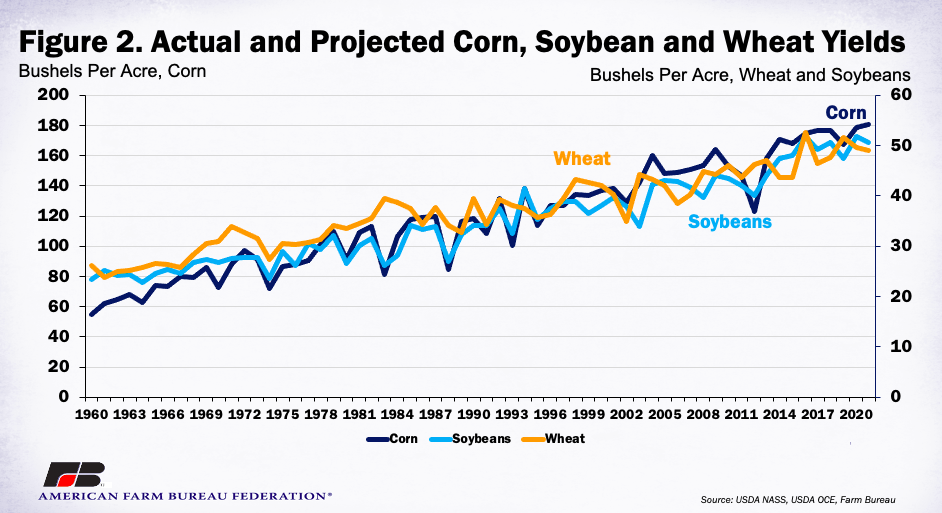

Corn yields for the 2021/22 marketing year are currently projected at a record-high 180.5 bushels per acre, 2.1 bushels per acre, or 1.2%, above the current marketing year. Soybean yields are projected to decline by 1.3 bushels per acre, or 2.5%, to 50.6 bushels per acre. If realized, 2021/22 soybean yields would be a tie for the second-highest on record. Wheat yields are projected to decline by 0.6 bushels per acre, or1.2%, below prior-year levels. Figure 2 highlights actual and projected corn, soybean and wheat yields.

Summary

USDA recently released a 10-year baseline projection including long-term supply, use and price projections for major U.S. crops and livestock products. Recent improvements in corn, soybean and wheat demand and prices are contributing to expectations that total acreage planted to these three crops will increase by nearly 7 million acres or 3%. Corn acres planted are projected at 90 million, soybean acres are expected at 89 million, and all wheat acres are expected at 46 million. Record yields are expected for corn, while lower crop yields are expected for both soybeans and wheat in 2021.

Updated expectations for corn supply and demand come quickly, with tomorrow’s WASDE widely expected to project increased demand and lower supplies for current marketing year crops.

Trending Topics

VIEW ALL