Farmers’ Losses a Barrier to PPP Participation

TOPICS

TaxesMegan Nelson

Economic Analyst

photo credit: Arkansas Farm Bureau, used with permission.

Megan Nelson

Economic Analyst

Since the Paycheck Protection Program’s inception, few farmers have been able to utilize the assistance offered, despite the efforts of the Small Business Administration to address all the potential questions that would arise when the application period opened (PPP Out of Funds, But Impact on Agriculture was Minimal). Of the $349 billion allocated to the PPP, it’s estimated that $4.374 billion, or 1.3%, was distributed to the agricultural, forestry, fishing and hunting subsector.

The SBA recently clarified that farm participation in the PPP is based on net farm profits (or losses), line 34, form Schedule F, from 2019. While the agriculture sector welcomed this clarification, many self-employed farmers are finding it to be a barrier to participation in the program.

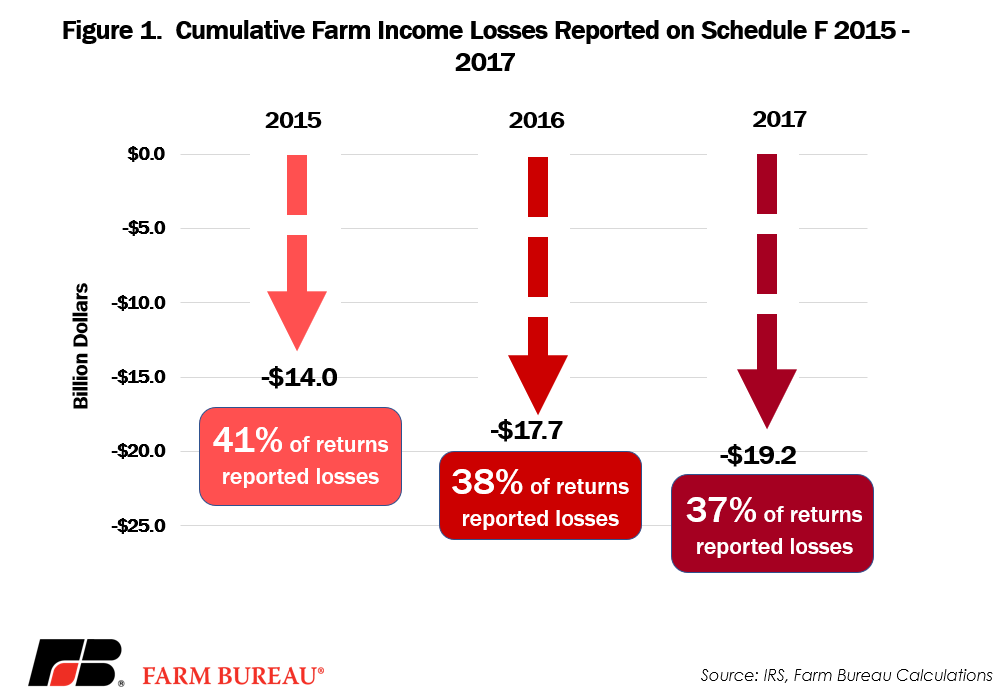

Based on 2017 IRS data, the most recent available, 37% of self-employed farmers would have not received a loan from the PPP because they’ve reported net losses in the prior year. Program eligibility is based on returns filed for 2019, so the percentage of self-employed farmers receiving a zero-dollar loan could be higher following devastating natural disasters and trade troubles that continue to weigh negatively on farm income and cash receipts.

Schedule F Trend

Farmers operating as sole proprietors determine their net profits or losses on the Schedule F tax form by inputting their annual farm business profits and subtracting expenses. According to the most recent IRS tax statistics, 1,789,262 Schedule F tax returns were filed in 2017, netting a cumulative loss of over $19.2 billion. For the same year, Schedule F cumulative farm losses increased 8.5% from 2016 levels and nearly 40% from 2015.

The IRS data categorizes the Schedule F returns only by adjusted gross income brackets and does not break down returns filed by commodity type or reflect any income that is reported via corporation or partnership. However, following the trend in Schedule F returns filed in 2017, net income losses would preclude 37% of farmers from participating in the PPP. The 2016 and 2015 percentages were similar, with 38% and 41% of the Schedule F returns showing net income losses, respectively.

Figure 1 shows cumulative losses reported on Schedule F from 2015 to 2017 with the percentage of returns reporting losses in each year.

Summary

The SBA’s Paycheck Protection Program was enacted to support small businesses during the COVID-19 emergency. However, impacts from natural disasters and other disruptions are likely to result in many farmers reporting net farm losses from 2019, making them effectively ineligible to receive a loan from the PPP, i.e., a zero-dollar loan. While farming operations will still be able to apply for a PPP loan based on any employee payroll costs, self-employed operators will not be able to access the PPP to pay themselves if they do not show a net farm profit in 2019.

In contrast to PPP, SBA’s Economic Injury Disaster Loan will be based on gross revenues, cost of goods sold, cost of operations, and other compensation sources for the 12-month period prior to Jan. 31, 2020. The SBA recently began accepting EIDL advance applications on a limited basis exclusively for agriculture. The EIDL will provide small business owners impacted by COVID-19 a loan of up to $10,000 that will not have to be repaid.

Trending Topics

VIEW ALL