August Cattle on Feed Report Moderately Bearish With Large Placements

TOPICS

Market IntelMichael Nepveux

Economist

photo credit: Colorado Farm Bureau, Used with Permission

Michael Nepveux

Economist

USDA’s latest Cattle on Feed report, released August 21, shows the number of animals on feed has moderately increased from 2019. The report provides monthly estimates of the number of cattle being fed for slaughter. For the report, USDA surveys feedlots of 1,000 head or more, as this represents 85% of all fed cattle. Cattle feeders provide data on inventory, placements, marketings and other disappearance.

August Cattle on Feed Report

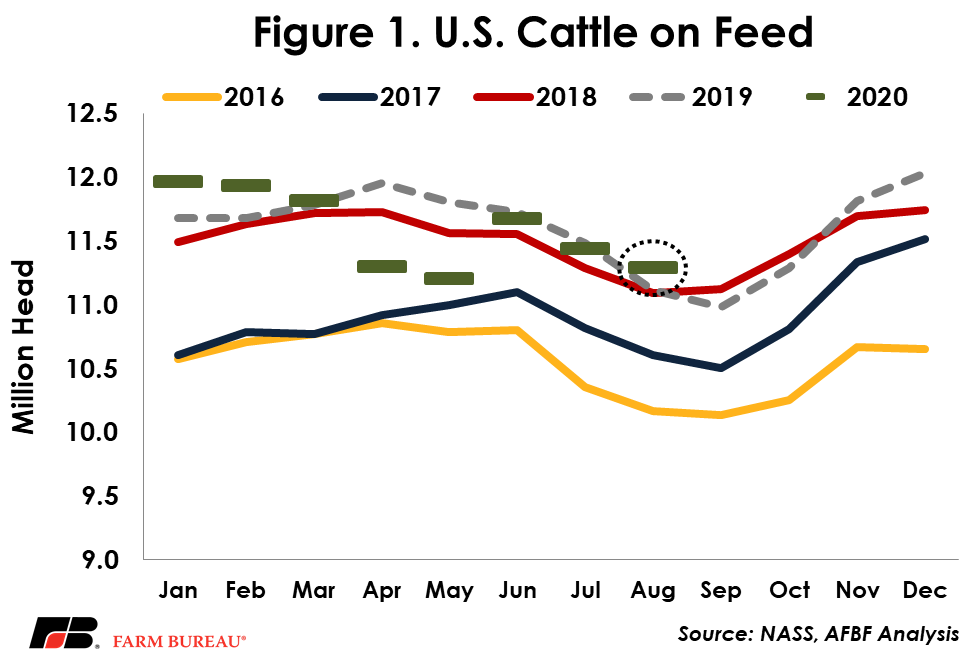

This report showed a total inventory of 11.284 million head for the United States on August 1. This 1.5% year-over-year increase is slightly above analysts’ expectations of an average increase of 0.7% in feedlot inventories. Smaller marketings and large placements pushed cattle on feed up 172,000 head over last year. This cattle on feed number is the highest ever posted for August since the dataset began in 1996.

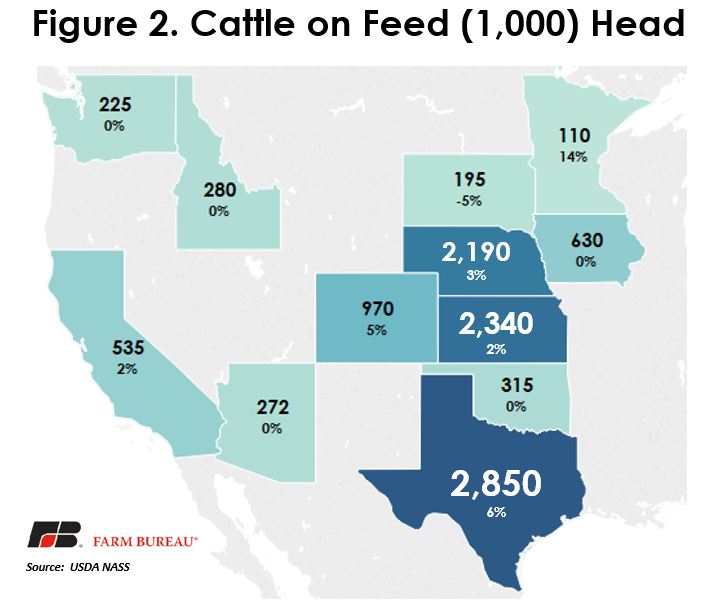

As usual, Texas, Kansas and Nebraska lead the way in total fed cattle numbers, accounting for nearly 7.6 million head, or approximately 64% of the total on-feed inventory in the country. Texas continued to gain year-over-year, adding 6% relative to 2019. Kansas also had a gain, adding 2% over 2019, and Nebraska reported a 3% increase.

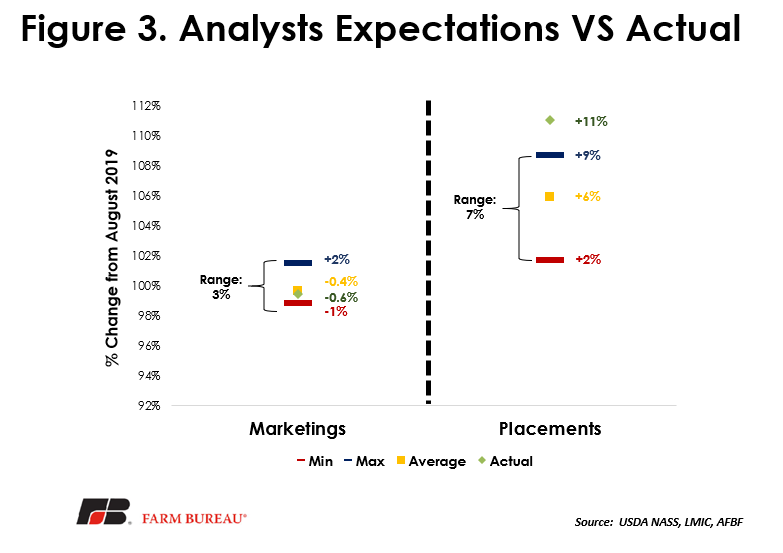

While total inventories are an important component of the report, other key factors include placements (new animals being placed on feed) and marketings (animals being taken off feed and sold for slaughter). Coming in at 11% over 2019, placements in July far exceeded both the average analyst expectation of a 6% increase as well as the maximum analyst expectation of an 8.7% increase. The relatively wide range of forecasts for placements -- 7% -- somewhat highlights the uncertainty that still exists in the market around the full impacts of COVID-19. Placements clocked in at 1.893 million head in July. Marketings largely fell within the predicted range at 1.990 million head, a small increase over year-ago levels.

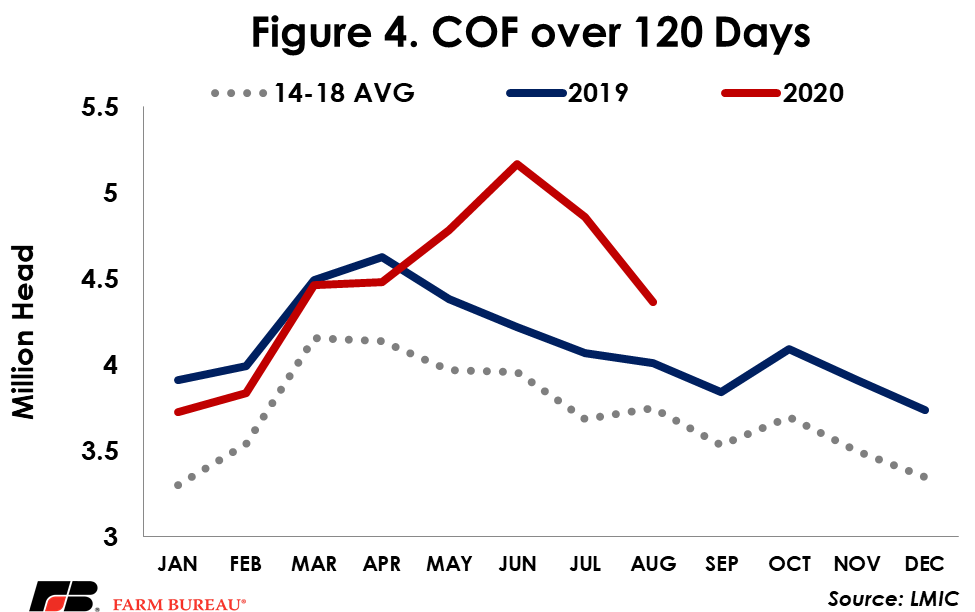

Placements were up across almost all weight categories. There was a slight decline in placements in the two categories above 900 lbs, which tells us we continue to work through the backlog of heavier animals resulting from the COVID-19-induced labor issues at processing facilities in early summer. July marked a month of progress for moving some of these heavier cattle off of pasture and onto feed, particularly in the Southern Plains. However, as Figure 4 shows us, we are still seeing very high numbers of estimated animals on feed over 120 days.

Summary

Overall, with plenty of animals in the pipeline for processing in the future, the August Cattle on Feed report is considered relatively bearish. However, the impacts of the processing disruptions in the early days of the pandemic are still reverberating, contributing to market uncertainty. Though it will still be a little while before the feedlot sector is current, there is a slight decline in the backlog from last month.

Trending Topics

VIEW ALL