Application Period Opens for Improved Round of Paycheck Protection Program

TOPICS

TaxesMichael Nepveux

Economist

photo credit: Right Eye Digital, Used with Permission

Michael Nepveux

Economist

The recently enacted COVID-19 resource and relief package included a number of agriculture-related provisions, such as a $1.5 billion extension of the Farmers to Families Food Box program, as well as additional support for crop, specialty crop, livestock, poultry and dairy farmers, among others, i.e., What’s In the New COVID-19 Relief Package for Agriculture? The bill also includes several improvements to a second round of the Paycheck Protection Program. Today’s article highlights the PPP improvements that will benefit farmers and ranchers, including new qualifying expenses, using gross farm income to determine loan amounts and reducing the level of required losses to qualify.

What is the Paycheck Protection Program?

The Paycheck Protection Program is basically designed to help small businesses remain in operation and keep their employees paid through this turbulent time. The program provides forgivable loans to small businesses to pay employees and keep them on the payroll. The program will provide to eligible businesses loans of up to $10 million to cover 2.5 times the average monthly payroll costs, measured over the 12 months preceding the loan origination date, plus an additional 25% for non-payroll costs. Payroll costs include salaries, commissions and tips; employee benefits (including health insurance premiums and retirement benefits); state and local taxes; and compensation to sole proprietors or independent contractors. Non-payroll costs include interest on mortgage obligations, rent and utilities. These loans have an interest rate of 1%, but the portion that covers eligible expenses is forgivable as long as the company maintains staff and payroll.

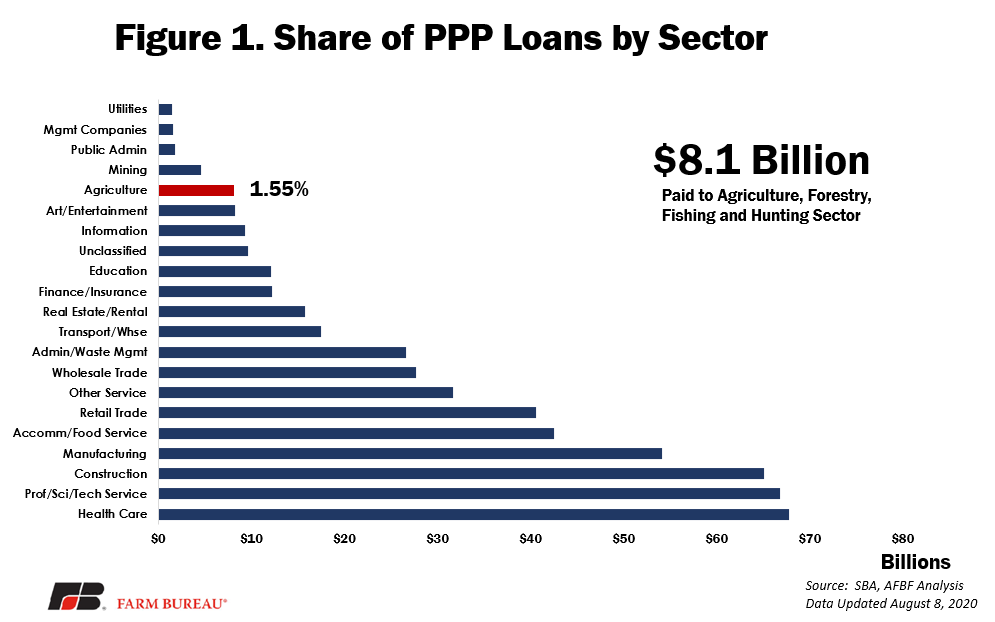

The Small Business Administration’s data on the program only covers loan disbursement through August 8, the deadline for the first iteration of the program. Under the first round of the program, 5.2 million loans were granted, resulting in $525 billion paid out. As Figure 1 shows, approximately 1.5% of these loans were paid to the sector (NAICS) that comprises agriculture, forestry, fishing and hunting. Approximately $8.1 billion was paid to this sector through almost 150,000 loans. The average PPP loan size across all sectors was approximately $101,000 dollars. At only $54,000 per loan, the agriculture sector’s average loan size was the third lowest.

What is Included in the Relief Package?

The legislation provides $284 billion in funding for a second round of PPP loans and several improvements AFBF advocated for. Among them is a clarification that allowable expenses that had been paid for with forgiven PPP loans may be taken as a business deduction for income tax purposes without limitation. This is an important distinction for farmers because the Treasury Department’s 2020 regulations denied PPP participants the ability to deduct these expenses, going against the intent of Congress. The bill also cut in half the qualifying reduction in gross revenue – dropping it from 50% to 25% -- between comparable quarters in 2019 and 2020. This much-needed change for producers who suffered multiple years of losses expands the number of farm and ranch families that can qualify to participate.

The changes to the expenses that the loans can be spent on and still be forgivable are also important. As mentioned above, previously the only approved expenses were payroll, mortgage interest, rent and utilities. Now, worker personal protective equipment and adaptive costs are approved expenses for loan forgiveness. The bill’s switch to gross income from net farm income for the loan requirement calculation for farmers and ranchers who file as sole proprietors will allow many more producers to participate. The previous net-farm-income-based method for establishing loans left many self-employed farmers ineligible because they had reported losses Additionally, producers applying for loan forgiveness under the program for loans under $150,000 will enjoy a new streamlined process.

What’s Next?

Last week, SBA announced that PPP lending would start on January 11 for borrowers new to the program; repeat borrowers can apply beginning January 13. The loan application deadline for the second round of PPP loans is March 31 or until funds are exhausted. Businesses with no more than 300 employees that received loans last year are eligible for this second round of PPP loans, but at a reduced loan cap of $2 million. Interested producers can visit the SBA website to begin preparing their application.

Trending Topics

VIEW ALL